A separate post makes the claim that working on ESG investing could be high-impact for people in the effective altruism community.

This article explores ESG/responsible investing in more detail. It identifies certain gaps which I believe could be valuably filled to help ESG investing do more good.

This report is for those who are interested in a career to influence the finance system. If you are interested as an individual investor, there are other resources (e.g. the report by Hillebrandt and Halstead or the CSP guide)

Note that I use the term ESG investing or responsible investing. The term impact investing risks being viewed as a niche pursuit for those willing to give up investment return in order to do good in the world.

The rest of this article is structured as follows

- Inwards/outwards impacts: excessive focus on impacts inwards

- Fiduciary duty exacerbates the “impacts inwards” problem

- Universal ownership can partially solve the problem

- Effective influence is possible

- Cause areas: the finance world has not chosen themes systematically

- Action: Which job to get if you want to take action

A number of appendices then explore a number of specific issues, such as how to balance divestment against engagement.

[Huge thanks to a number of people for helpful conversations and for reviews of various drafts of this post; particular thanks to Ellen Quigley for a number of helpful conversations, and many helpful comments and improvements to this post. Also many thanks to Eric McKay, who highlighted to me the importance of engagement. Thanks also to Jonathan from TPP, Marek, Meg, Grayden, JueYan, Ashok from EMIA, and others. Any errors are mine]

1. Inwards/outwards impacts: excessive focus on impacts inwards

When I refer to “impacts inwards” I mean the risks to a company (or to any issuer of shares/debt/other security, i.e. not necessarily a company). An “impacts outwards” mindset is about the risks that are brought about to the wider world by the company/issuer.

The financial world is dominated by the “impacts inwards” mindset. The financial world is used to the question: will I, the investor, get a good return on my investment? Indeed some would say that ESG investing is *defined* this way.

However the “impacts inwards” mindset is not well aligned with ensuring that responsible investment/ESG investment actually leads to the world being significantly better. Under the “impacts inwards” mindset, it is entirely consistent that “Exxon built rigs to account for climate change-related sea rise while funding climate change denialism research” (quoted from Quigley et al 2020, which cited Oreskes and Conway 2010). It helps us understand why BAT can have award-winning sustainability ratings, despite selling a product which kills.

Despite increasing recognition of what is referred to in the sector as “double materiality” (i.e. the idea that we need both “impacts outwards” as well as “impacts inwards”) the “impacts outwards” are still secondary.

Given that “impacts outwards” are not given enough attention, we currently have a lot of issues which, if addressed, could enable the world of finance to achieve much more impact

- Universal ownership gives even those with a “impacts inwards” mindset a reason to incorporate “impacts outwards” thinking

- This creates a number of important tasks around quantitatively modelling impact

- This may require the finance sector to develop a relatively novel skillset, namely the ability to combine standard financial modelling skills (already widespread in the finance sector) and understanding of impact

I’m not claiming that “impacts inwards” thinking is the only thing that has held the finance sector back from achieving more positive impact on the world, only that it’s a material factor.

2. Fiduciary duty exacerbates the “impacts inwards” problem

Pension schemes are bound by a requirement called fiduciary duty. (To understand more about why pension schemes are important, see the map of different players in the financial space in the section on how to take action). This is a legal requirement which is imposed on pension trustees. In the UK it requires them to ensure the solvency of the pension scheme. They are allowed to consider ESG factors when investing, but not if doing so will materially conflict with delivering investment returns. This is a barrier to incorporating impact considerations when investing. Remedying this (and note that the UK charity ShareAction is working on remedying this) will require a change on the part of the relevant state apparatus, such as the DWP in the UK. I am less familiar with how fiduciary duty works in other jurisdictions.

The issues around fiduciary duty are potentially worrisome. Pension schemes are very important asset owners, and while the standard techniques of engagement and divestment can influence outcomes at the level of the companies/entities they invest in, there is a limit to what they can achieve if asset owner appetite for change is limited by fiduciary duty.

I’m not claiming that fiduciary duty is the sole cause of excessive focus on impacts inwards. While removing the barriers of fiduciary duty will not be enough to radically change the system, it will likely help.

In the meantime I do believe that there’s enough momentum behind the ESG concept that the sector will be willing to incorporate ESG factors to the extent that they fit into the profit-focused paradigm. The way the sector is heading now, investors will think about the ESG factors relating to a company if it helps them make better decisions about whether they will make money by investing in that company.

I’m excited by a world in which the financial world does properly account for externalities, and I’ve set out more thoughts on what this could look like in Appendix 4.

In the next section I set out an approach which is sufficiently ambitious relative to what’s happening currently to make a big difference, and yet realistic given the modes of thinking that are current in the financial system. This approach is called universal ownership.

3. Universal ownership can (partially) solve the problem

Universal ownership is an exciting concept which may be consistent with fiduciary duty (based on my understanding of a discussion of this at symposium in Jan 2021)

Here is a summary of the concept behind universal ownership:

- Imagine you’re a “universal owner” (i.e. an investor with broad exposure across the whole market)

- Imagine your portfolio includes a “bad egg”, meaning a company with substantial negative externalities (e.g. a fossil fuel company with aggressive lobbying practices, say)

- Those “bad eggs” cause various bad effects, some of which may be economic, e.g. causing the other companies in the portfolio to suffer losses in the future

- This means you may be willing to incur a loss of (say) 50% on the value of the bad egg in order to achieve a benefit of (say) 3% on all of the rest of the portfolio, meaning that the overall portfolio doesn’t lose money

The numbers 50% and 3% in the previous example were made up; a valuable piece of work to be done is to work out what those numbers might look like based on actual portfolios.

To my knowledge nobody has been doing these calculations, however I believe that they could be valuable and instructive.

Note that I refer for the sake of example to “bad eggs”. However it doesn’t matter how bad the company’s externalities are. What’s really important is whether you, as an activist shareholder, could ask the company to change its behaviour -- even if that causes a reduction in the return for that company -- but could bring about improvements in the externalities for the rest of the portfolio.

Anticipating objections/queries:

- Is it realistic for any one shareholder to really be able to have enough influence to change the bad egg’s behaviour, especially if the bad egg is a big company?

- Yes, but only if it’s the right shareholders. A large asset manager like Blackrock or Vanguard likely already owns around 5% of the company, even if it is a large company. This is big enough that the company is probably already having regular meetings with the CEO/senior management team of the firm.

- A few tangible examples:

- Is there a tragedy of the commons risk? I.e. is it not better for any one asset owner/manager to divest from the bad egg and benefit from the improvement to the rest of the portfolio?

- Possibly. This could be a potential downside from the association between divestment and “doing good”.

- However for large asset managers this is harder to do. As Ellen Quigley notes in her paper on Universal Ownership, “For very large investors, exit is difficult because the act of selling a large block of shares can affect prices.” I would add that if “very large investors” means asset managers like Blackrock and Vanguard, they have a number of client needs to meet, so wholly divesting means engaging with a number of clients, which would be difficult. Quigley continues: “For universal owners, then, liquidity is mainly a hypothetical concept. In practice, they tend to behave more like investors in illiquid markets – they default towards active ownership.” She cites McNulty & Nordberg (2016).

- Does this not miss out the non-economic issues?

- Yes, it does. It still means that, for example, to the extent that animal welfare issues (say) don’t impact on the profitability of firms or the wider economy, ESG investing can only ask for changes which don’t cause much financial harm.

- However, given the profit-focused mindset and the fiduciary duty constraints set out in the previous section, I believe this is still the most ambitious ask that is realistic.

- Could this be contrary to antitrust rules?

- Thank you to JueYan for mentioning this risk to me

- I haven’t looked into this, but I’m hopeful that the momentum behind ESG investing will help overcome any issues here

- If the externalities in question aren’t being explicitly modelled, is it possible to incorporate the benefit from avoiding them in valuations?

- Let’s focus the conversation on climate change, as I think this is the context where Universal Ownership is most likely to be actually implemented (at least at first)

- When firms are valued, there is not typically an explicit adjustment for climate-related risks (except perhaps for companies which are particularly obviously exposed to climate risks)

- However arguably they are incorporated in the discount rate

- This lack of explicit accounting would certainly make it harder to account for the benefit of avoiding externalities, however as long as the externalities are real, it should be possible to incorporate them. This may mean explicitly modelling the risk that explicit adjustments for climate risk *will* be added to models at a later date.

I would recommend that interested readers review Ellen Quigley’s 2020 paper: “Universal Ownership in Practice: A Practical Positive Investment Framework for Asset Owners”. The paper covers a broad range of relevant topics in addition to the specific content discussed above.

There are also a number of innovations in ESG thinking which become possible within the universal ownership structure. For example, ESG investing has tended to focus its attention on the most obvious “perpetrator” of problems. In the case of climate change, the focus is on supply (fossil fuel companies) with no attention to demand (e.g. cement, steel, cars, flights). Furthermore, oil and gas financing has largely come from bank loans and underwriting (Quigley 2020). Asset owners with exposures to commercial banks could insist that the bank no longer funds fossil fuels, and this is an ask that is not too demanding for the bank because it tends to account for a modest proportion of its lending book.

Note that this section assumes that it *is* possible for investors to influence the companies that they invest in.

4. Effective influence is possible

There is already a substantial literature on how investors can have an influence on the companies/entities they invest in.

The two main tools in an investor’s toolkit are divestment and engagement. For brevity I won’t go into this here, although I do discuss it in an appendix.

The only important point for the main thread of this argument is that it is possible for an investor to have effective influence over a company they invest in.

Based on Quigley et al's report on whether the University of Cambridge’s endowment should divest from fossil fuels, it seems that shareholder/investor engagement is often ineffectual, focusing often on relatively undemanding asks, such as disclosure (despite the fact that studies seem to suggest that greater disclosure does not reliably lead to real world outcomes, such as improvements in environmental performance). Furthermore the mechanism employed is typically shareholder resolutions, which are often not successful and frequently don’t lead to implementation.

Promisingly, however, the report does set out what effective engagement could look like:

- Set out asks that are truly effective in making the world a better place

- Employ effective incentives to engender implementation, such as voting against the re-election of directors who oppose the changes (also called “vote-no”), or building effective outcomes into remuneration structures

This seems to suggest that engagement could be an effective tool. This is corroborated by Naaraayanan et al 2019, which explored the work of the Boardroom Accountability Project, and concluded that it was effective at achieving real world outcomes.

5. Cause areas: the finance world has not chosen themes systematically

To my knowledge nobody is trying to systematically consider the question of which cause areas are the most important ones to tackle for responsible investors.

(One person I spoke indicated that The Investment Integration Project was doing this, however when I consulted their website I couldn’t find any sign of them systematically or rigorously prioritising between cause areas. I also hear frequent references to the SDGs, however this does not help us to prioritise which cause areas are most important. Furthermore some themes, for example AI risk, may need a bit of squinting before they can be shoehorned into the SDG structure.)

Here I set out some tentative opinions about cause areas that need further attention in the world of ESG/responsible investing. This section has not been carefully researched and I would like to see more research conducted on this.

Climate change: climate change needs no additional attention. The discourse around ESG investing is already heavily focused on climate change. In its favour is the fact that effective responsible investment could be “make or break”. I.e. financing decisions could easily make the difference for whether new fossil fuel facilities are brought about, and this would have a material impact on whether we reach our Paris targets.

AI risk: Despite the risks from AI, I don't see any benefit in denying debt for AI related projects -- AI has many upsides. However an engagement strategy which makes AI safety an agenda item for conversations with management of (e.g.) Alphabet has merit. There are some who are concerned about AI as an existential risk, and this may seem radical in most finance discussions. However talking about the risks that AI and algorithms could have on political polarisation and other areas of life has intrinsic merit and could fall on a spectrum with the more existential risks. I don't expect the impact of effective ESG finance to be “make or break” for AI risk, but providers of finance could be highly influential in setting the agenda.

Animal welfare: Factory farming falls firmly in the remit of corporate behaviour. Radically ambitious demands may be unrealistic given the challenges relating to fiduciary duty. This does not mean that there's no scope for action however. Indeed I understand that there is a relatively modest difference in cost between the worst factory farms for hens and a cage-free approach. This means that relatively light touch advocacy and engagement on the part of asset managers could be quite influential. While on balance I’d expect that any factory farming successes achieved by effective ESG investment would be in part due to the lobbying done by NGOs, I think that if the world of finance can be made to make this a priority, this would be a strong exciting opportunity for change.

Global conflict: Many European investors already don't invest in arms manufacturers. Furthermore if private sector investment dried up governments would likely still be a source of finance. I still think there is some scope for positive influence, but I wouldn’t consider this as being among the more promising topics for responsible investment.

GCBRs (Global catastrophic biological risks) and pandemic risk: Pandemics can be "natural" or engineered. Natural pandemics are exacerbated by human behaviours such as flying (which spreads pathogens quickly) and deforestation (which exacerbates zoonotic disease). While viewing these risks through a pandemic lens may add value in an ESG context, these exacerbating factors are also risk factors for climate change. At first glance it therefore seems that responsible investors may be adding little value by considering the pandemic risks which arise from deforestation or aviation. Having said that, where models are being used to *quantify* the benefits/harms of corporate activities (which isn’t really happening yet), adding pandemic risk to the climate change risk could be material enough to influence decisions. Also issues around lab safety and the careful management of the risks from biotech firms could conceivably be a valuable source of influence. In practice, I am quite positive about responsible investment strategies having a focus on pandemic risk in the short term. This is because (a) it could be adhered to with relatively little extra effort, given the material overlap with climate risk (b) there’s material impact to be had by demonstrating that there are other risks for responsible investment strategies to consider other than climate risk.

Global poverty and health: The financial system invests in sovereign debt as well as corporates and therefore has influence over governments, including governments in the developing world. While enlightened leaders of developing world nations are already intrinsically incentivised to improve the lot of their poorest people, there may be benefits in providers of finance demonstrating that helping the poorest of the poor matters to them too.

I believe that a thoughtful application of the I-T-N (Importance, Tractability, Neglectedness) framework within the context of ESG investing could be powerful for making these assessments more robust.

6. Action: Which job to get if you want to take action

This section could be useful for you if you are inspired to pursue the ESG/responsible investing concept, and are either already working in finance and considering your next move or considering where to start your career in finance

- 5.1 Map of areas to work in finance

- 5.2 Tentative opinions on which areas are most valuable

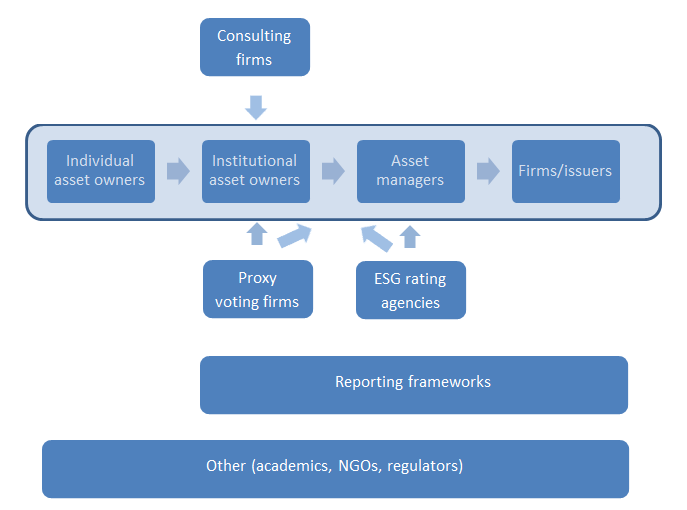

6.1 Map of areas to work in finance

Individual asset owners include normal individuals like you and me. They might also include companies. Their money gets aggregated together in various ways, so that institutional asset owners then have control over the funds. Examples of institutional asset owners include pension funds, the annuity portfolios and other savings-type portfolios held by life insurance companies, and commercial banks. The institutional asset owners I have in mind have some degree of control or responsibility for how the funds are managed. For example, they might set a mandate, or make high-level decisions about how funds are managed. Those funds are then typically managed by asset managers. Asset managers include the likes of Blackrock, Vanguard, Fidelity, and State Street. They make decisions like how much to invest in any particular company. They will often also manage a relationship with a company in their capacity as a significant shareholder or debtholder. An asset manager as large as those named earlier may have a stake as large as 5% or 10% in even the largest of firms. Individuals can also access asset managers directly and bypass institutional asset owners.

An important component of asset owners is the pension schemes, where the ultimate decision-makers are pension scheme trustees, who are typically employees of the company and often don’t have expertise in finance. Pension schemes are supported by pension fund consultants. Consultants to asset owners are typically firms of actuaries. Such companies may also provide consulting services to life insurance companies (the other material type of asset owner), since the actuarial skills required are similar. I’m basing this on my experience in the UK; I haven’t checked to what extent this applies in other jurisdictions.

An important party in between the asset owners and the asset managers are ESG ratings agencies. These include, for example, MSCI and Sustainalytics. As an asset manager you will often not have capacity to expend great care and thought over ESG factors, especially if each analyst has many companies to oversee, and already plenty of work to do just thinking about standard considerations like profitability, so you will likely rely heavily on ratings provided by these companies.

There are currently a number of reporting frameworks, such as SASB (Sustainability Accounting Standards Board) or GRI (Global Reporting Initiative) or TCFD (Taskforce on Climate Financial Disclosures). These frameworks govern the information provided by companies about ESG, i.e. they govern their disclosures. SASB strikes me as particularly exciting because it feeds into ISS (see below). These frameworks tend to focus on the risks that negative externalities (such as climate change) impose on the company in question (i.e. impacts inwards), and not risks that these companies pose to the system as a whole, or impacts outwards (Quigley, 2020).

Proxy voting firms are helpful for asset owners who don’t have the capacity to carefully review the resolutions at each AGM themselves -- which would be the case for any pension fund. The proxy voting firm can vote on their behalf. The company which has the largest market share is ISS. Others include Glass Lewis and Egan-Jones. Making proxy voting firms more effective could be powerful or engendering more impactful engagement.

NGOs include Majority Action in the US, ShareAction in the UK, Banktrack in the Netherlands. A newly founded, lesser known example is the Emerging Markets Investors Alliance that I’ve recently come into contact with. These NGOs typically seek to influence various of the above-mentioned parties through their campaigning/influencing.

Note that I’ve focused this depiction of the landscape on what’s called the “buy-side”. There is another landscape called the “sell-side”. This is the side which is important when companies are issuing debt or equity, and is dominated by investment banks. I have omitted this because I expect the sell-side to follow the lead of the buy side. I believe the sell-side (i.e. investment banks) could become incredibly important if/when we need to explicitly and quantitatively incorporate ESG factors into company valuations.

I have not included retail/commercial banks in this outline because I don’t know them as well. However I know that a huge amount of current financing of oil and gas financing comes from bank loans (source: Quigley et al’s divestment report, p87) so I’m tentatively positive about people working here.

6.2 Tentative opinions on which areas are most valuable

This is an assessment of where to work if you want to do good with your career. A number of judgement calls have been made in creating this list, and I believe the assessments could be improved by expanding the list and giving the assessments more thought.

| Institutional asset owners | ★★ | Management of pension schemes is largely outsourced to an actuarial consultancy. However working on asset strategy in a life insurance company is an option. This would likely be working on something called “ALM” or asset liability management, and you would probably need to qualify as an actuary in order to do this. I think this role could have potential to drive forward an effective ESG agenda. Would only relate to the assets of one insurance company though (could be c£100bn, for a medium-to-large insurer). In addition, your ability to influence asset managers might be limited if your life insurer has an in-house asset manager (as is common) -- this means you can’t influence any asset manager other than your in-house one. |

| Asset managers | ★★★ | Ultimately asset managers are crucial, and success will be achieved when asset managers are implementing ESG investing in an impactful way. The only reason for giving this a lower rating is that I think it’s too soon. Lots needs to happen on the side of clients of asset managers first. However working at an asset manager now so that you can have impact later could be an excellent strategy and I very much hope that some people will do that. |

| Consultants to asset owners | ★★★★ | A consulting firm could have influence over large numbers of pension schemes (and potentially other asset owners too, depending on the consulting firm). And the demands being made by asset owners are central to shaping the way that asset managers behave. So this strikes me as a very high impact area to work. |

| ESG ratings agencies | ★★★★★ | Asset managers are mostly heavily reliant on ratings, especially those from MSCI and Sustainalytics. This means that adjustments to these ratings would likely have a huge ripple effect throughout the sector. |

| Reporting frameworks body | ★★★★ | The rare asset managers who are not heavily reliant on ratings will likely need to lean on the information provided by the company being analysed, which in turn will be driven heavily by the disclosures set by the likes of SASB or GRI. While asset managers are not currently leaning heavily on these frameworks, I suspect that successful evolution of ESG investing will require these frameworks to consider impact carefully. |

| Proxy voting firms | ★★★★★ | Voting firms like ISS are hugely influential. Many pensions schemes/asset owners will rely entirely on a proxy voting firm. Even the stewardship departments of a large asset manager like BlackRock will subscribe to ISS etc and take their guidance into account. |

| Other | ★★★★ (?) | There is a mixture of things here, which makes it harder to give a confident assessment, however having an NGO working from the outside of the system certainly could, in principle, be very valuable. |

Appendix 1: Exploring divestment and engagement

- Appendix 1.1 A list of theories of change

- Includes the divestment/cost-of-capital theory of change and engagement

- Appendix 1.2 Which distinctions are useful in choosing the best theory of change?

- I consider the primary/secondary distinction, but decide that a debt/equity distinction is more useful

- Appendix 1.3 Some tentative conclusions on the optimal approach

- “Engage in equity, deny debt”

Appendix 1.1 A list of theories of change

Appendix 1.1.1 “Cost of capital” theory of change

(1) INVESTOR INVESTS/DIVESTS --> (2) CHANGE IN COST OF CAPITAL --> (3) COMPANIES ARE MORE/LESS ABLE TO DO GOOD/BAD THINGS

Most of the discourse on ESG/responsible investment is characterised by an excessive focus on divestment from publicly traded equities (stocks and shares). Many in the sector would, if pressed, indicate that its theory of change looks like this:

(1) INVESTOR INVESTS/DIVESTS --> (2) CHANGE IN COST OF CAPITAL --> (3) COMPANIES ARE MORE/LESS ABLE TO DO GOOD/BAD THINGS

The evidence does not appear favourable towards this theory of change.

In this section, I set out some reasons to doubt this theory of change. I am not actually confident in the conclusion that this divestment mechanism is ineffective, however I do believe that effective divestment from publicly traded equities is likely to be less effective than effective engagement on publicly traded equities.

Quigley et al's report on whether the University of Cambridge’s endowment should divest explores in some depth whether divesting from publicly traded equity (i.e. shares) is effective with respect to this theory of change. The report suggests that this theory of change has not been effective thus far when it comes to publicly traded equity.

It argues that

- Divestment appears to have little effect on share price

- During the beginning of the Apartheid South Africa divestment movement in the early 1980s, around $7.6 billion USD was invested in South African companies’ shares (Gosiger 1986, 519); despite this volume of securities ownership, the divestment campaign itself had an indiscernible effect on share prices for South African companies (Ansar, Caldecott, and Tilbury 2013; Teoh, Welch, and Wazzan 1999)

- Most responsible investments “promise only modest and perhaps even negligible investor impact” (Kölbel et al. 2020)

(Each bullet point is a quote from Quigley et al’s divestment report; I would encourage interested readers to read Appendix IV which I have found to be very useful)

Note also that under this theory of change it’s the cost of capital which is influenced, which means that it’s harder (but still not impossible) for the negative-externality-laden company to find funds for *future* activities. While influencing yet-to-be-financed activities is potentially powerful, it would be better to be able to *also* influence already-financed activities (see section on engagement later).

A depressed share price has unclear implications for management incentives.

Let’s say that divestment *has* successfully increased the cost of capital (i.e. reduced the price of the security). Does this improve incentives for good management decisions? Probably not, it seems.

Quigley et al quote Davies and Van Wesep 2018 observing that “under typical compensation schemes, managers seek to maximize stock returns, not stock prices”. I.e. as an exec of a large company, you are both a buyer of the company’s stock (when you receive it) and a seller of the company’s stock (some time after you’ve received it). So if the divestment effect is a temporary reduction in share price, company managers typically benefit from the share price being depressed (unless they plan to sell shares imminently). Davies and Van Wesep note that it is possible to restructure compensation packages to make them more susceptible to the effects of divestment campaigns, however this happens by making them more short-term-focused, and incentivising managers based on long term outcomes is generally considered to be more consistent with good governance.

Another potential objection is called the Green Paradox. If divestment from (e.g.) fossil fuels is loud and visible, fossil fuel companies may respond by accelerating fossil fuel extraction, which could make things worse. In Appendix 2 I discuss why this appears not to be material.

In Appendix 3 I explore further whether this theory of change really is ineffective.

Appendix 1.1.2 “Automatic” theory of change

The most naive theory of change is

DENIAL/DIVESTMENT-> ACTIVITY LESS LIKELY TO HAPPEN, or (conversely)

INVESTMENT->ACTIVITY MORE LIKELY TO HAPPEN

We need to distinguish between

- the primary market, where investing actually leads to money going to the company (or government or other entity)

- The secondary market, where you are buying an asset from another investor

In the case of assets on the secondary market the automatic theory of change represents a naive misunderstanding. The company has already received the funding for that activity: divestment or investment will not change that fact.

For the primary market, the extent to which this is impactful depends on how well subscribed the asset is (i.e. are there lots of other people prepared to invest).

Appendix 1.1.3 “Social license” theory of change

Quigley et al's report on whether the University of Cambridge’s endowment should divest explores in some depth whether divesting from publicly traded equity (i.e. shares) is effective with respect to the following theory of change:

(1) INVESTOR DIVESTS --> (2) LOWER MORAL CREDIBILITY/SOCIAL LICENSE → (3) POTENTIAL LEGAL/REGULATORY CHANGES

Some citations in Quigley et al’s report lean on Blondeel 2019, which analyses the Fossil Fuel Divestment movement through a neo-Gramscian lens.

Quigley argues that this theory of change can be effective.

Appendix 1.1.4 “Engagement” theory of change

Engagement here refers to asset managers using their position of influence as owners (or providers of finance) to bring about better behaviour on the part of the company.

The theory of change for engagement is simpler for an asset manager:

ASSET MANAGER EMPLOYS EFFECTIVE ENGAGEMENT → FIRM CHANGES BEHAVIOUR

For an institutional asset owner, the theory of change for engagement has an extra step:

ASSET OWNER DEMANDS EFFECTIVE ENGAGEMENT → ASSET MANAGER EMPLOYS EFFECTIVE ENGAGEMENT → FIRM CHANGES BEHAVIOUR

Quoting from Quigley et al's report on whether the University of Cambridge’s endowment should divest from fossil fuels, it seems that shareholder/investor engagement is often problematic, focusing often excessively on relatively undemanding asks, such as disclosure, and often also ineffective.

Promisingly, however, the report does set out what effective engagement could look like:

- Set out asks that are truly effective in making the world a better place

- Employ effective incentives to engender implementation, such as voting against the re-election of directors who oppose the changes (also called “vote-no”), or building effective outcomes into remuneration structures

- Ensure that major shareholders (such as large asset owners like Blackrock and Vanguard) themselves have the right incentives to implement these effective measures

This seems to suggest that engagement could be an effective tool. This is corroborated by Naaraayanan et al 2019, which explored the work of the Boardroom Accountability Project, and concluded that it was effective at achieving real world outcomes.

Appendix 1.2 Which distinctions are useful in choosing the best theory of change?

A sophisticated responsible/ESG investment strategy could employ different methods in different contexts. How should we distinguish which methods (i.e. divestment versus engagement) apply in which contexts?

Appendix 1.2.1 Primary/secondary distinction

The above reasoning suggests that the optimal strategy may depend on whether the investment is happening in the primary or secondary market.

This seems seductive and was initially how I thought about this. However it suffers from a fatal flaw.

If there is appetite to purchase “bad” securities on the secondary market but not on the primary market then it really only needs a very tiny number of investors who are willing to purchase stocks on the primary market in order for there to be no impact on the cost of capital. This is because those who purchased the asset when the finance was issued (i.e. on the primary market) can immediately sell it again on the secondary market and make a huge profit. This potential for gain will push the price on the primary market close to the price found on the secondary market.

This flaw may not be so fatal in cases where there are sufficiently significant structural differences between investors in the primary and secondary markets, however I don’t know of assets where this is the case.

Appendix 1.2.2 Asset classes

There are some who argue that we should “engage in equities, deny debt”. I understand this phrase is due to Andreas Hoepner (thank you to Ellen Quigley for bringing this to my attention)

Having a strategy which differentiates along the lines of asset classes (equity v debt) rather than following the primary/secondary distinction makes sense because of publicity, and because of debt not typically being permanent.

Issuance of equity typically is subject to much more publicity. An IPO (Initial Public Offering) will likely involve press releases and large amounts of public disclosure. Issuance of debt is different. Companies may borrow from banks. They may also borrow from the capital markets which typically involves dealing with an investment bank who in turn sells the debt via a process called syndication. Syndication often works based on networks and private conversations.

This has caused companies conducting activities which are frowned upon (e.g. tobacco or fossil fuels) to be more prone to raise money from debt than equity.

Furthermore, as Hoepner points out, debt has to be re-issued regularly, whereas shares are permanent. At any one point in time, a company will likely have some of its debt, maybe most of debt, up for renewal within a small number of years, at which point the company is going back to the primary market. Denying debt on the primary market has more impact than on the secondary market.

Appendix 1.3 Some tentative thoughts on how to choose between different approaches

An investigation which I think is crucial and which I haven't yet seen is a quantitative comparison between the “social license” theory of change and the “engagement” theory of change.

Divestment in order to impair the social license to operate seems to have some impact. Effective engagement seems to have some impact. One investor can’t do both. Which will have more impact?

My opinions on this are quite caveated. However here are some thoughts:

- Engagement has a fairly direct link between action and results (you ask for something and hopefully get it) whereas modifying the social license to operate is quite indirect.

- I think the Quigley divestment report does make some strong arguments suggesting that the first step in the theory of change ((1) INVESTOR DIVESTS --> (2) LOWER MORAL CREDIBILITY/SOCIAL LICENSE) can be effective; indeed Quigley quotes the chair of the UK Oil and Gas Authority (OGA) saying “its [the industry’s] social licence to operate is under serious threat”.

- The second step ((2) LOWER MORAL CREDIBILITY/SOCIAL LICENSE → (3) POTENTIAL LEGAL/REGULATORY CHANGES) is less clear to me.

- I suspect this step is real, however perhaps there are ways to achieve this without robbing responsible investors of the opportunity for influence.

- In the specific context of climate change, I would need more evidence to believe that further threats to the social license of fossil fuel companies outperforms effective engagement with those companies

- For a more immature topic, raising the profile of the topic may have more publicity value

- Engagement is likely more effective for shareholders than debtholders (because shareholders own the company)

- The appropriate strategy likely depends on the asset manager. For a large asset manager like BlackRock, the tractability of divesting from any one large company may be so low that engagement becomes more credible. This is intractable because it may mean restructuring expectations with clients and because selling large blocks of business can move prices (this point is also discussed in the section on universal ownership)

- For a relatively immature theme (i.e. a topic which hasn’t yet been discussed much in the world of ESG investing), divestment actions may be more valuable because they can set the tone for future engagement. If (e.g.) BlackRock raises the topic of animal welfare in a conversation with (e.g.) a major fast food chain, the company may assume that the conversation is unimportant if it has never influenced an asset allocation decision.

The below table tentatively sets out an approach which incorporates the above considerations.

Mature ESG theme (e.g. climate) | Immature ESG theme (e.g. factory farming) | |

| Equities | engage | deny/divest (?) |

| Debt | deny/divest | deny/divest |

An alternative approach (which may turn out to be similar)

| Any ESG theme | |

| Equities | engage (with threat of divestment) |

| Debt | deny/divest |

To get a better handle on this, I’d like to see more research about how government policymakers are influenced. Specifically I’d like a model (however rough) which could allow an estimate of how material the impact of the divestment decision would be as a function of how high profile the divestors are, how “noisy” the divestment is (e.g. how much PR there is around it) and the wider context. While I believe that the social license theory of change does achieve something, more research would be useful for understanding what the effect size may be.

To conclude this section, it’s important to highlight that debt is neglected, has scale, and is a much easier asset class to make traction in, because the optimal approach is around asset allocation, which is a more natural way of thinking about ESG investing than engagement.

Appendix 2: The Green Paradox

- Divestment is more effective at lowering prices when there is more attention/publicity

- Divestment is more effective at lowering the social license to operate when there is more attention/publicity

However, a downside of publicity is that it engenders the Green Paradox for certain topics.

“The Green Paradox describes the observation that an environmental policy that becomes greener with the passage of time acts like an announced expropriation for the owners of fossil fuel resources, inducing them to accelerate resource extraction and hence to accelerate global warming.” (source: wikipedia)

Specifically, this applies for any cause areas where real impact would result in a form of expropriation from the current owners, where the impact will take time to occur, and where, during that time, there is scope for current owners to accelerate their externality-generating activities. Clearly this problem applies (in principle) for fossil fuel extraction, for example.

However Bauer et al 2018 argue that the positive divestment effect wins over the Green paradox under reasonable assumptions.

Furthermore, it seems likely that if fossil fuel companies *did* worry that the cost of capital was going to increase, this would be more likely to engender a Green Paradox than investor engagement.

Appendix 3: Is the cost of capital theory of change for divestment really ineffective?

At first blush, the idea that divestment would have zero effect on the cost of capital sounds overly harsh -- ultimately the price is determined by supply and demand, and if you affect demand, the price should change.

Some observations on this

- The key conclusion is that divestment underperforms engagement when it comes to publicly traded equity; this doesn’t need us to prove that it has zero impact

- Quigley’s divestment report suggests that divestment may have some impact on share price, however it tends to be short-lived

- This short-livedness makes sense given that the true fundamental value of a stock is based on its future cash flows, which should win out in the end

- I would have more confidence in this conclusion if we could confirm that there is quickly-diminishing-marginal-price-impacts on there being another investor:

- Imagine going from zero investors to there being one investor: this has a huge effect on the price -- it goes from infinity to some price

- Now imagine going from one investor to two investors: this also has a big impact because two investors can bid against each other, which doesn’t happen in a monopsony

- Presumably going from two investors to three investors is less substantial a price impact

- If we could verify that this curve diminishes quickly (i.e. after a fairly small number of investors) then this could indicate price impacts would likely be minimal unless we achieved the highly unrealistic goal of (voluntarily) stopping all (or almost all) investment

- Quickly diminishing marginal price impacts would be more likely to apply where the true value (i.e. the present value of the future cash flows) is easier to discern

Could the scale of the divestment be relevant?

Some of the evidence cited in (e.g.) section 1 of this report (see Hansen and Pollin 2018) refers to what has happened in the past in a climate/fossil fuels context. Hansen and Pollin review Dordi and Weber 2019 and point out that while Dordi and Weber do conclude that their “results suggest that prominent divestment announcements have a statistically significant negative impact on the price of fossil fuel shares”, the effects they observe are “short-term, modest and inconsistent”. They continue: “in terms of one-day impacts only, they find that only 14 of the 24 events registered any statistically significant impacts on fossil fuel share prices, with 10 of the 24 events exerting no statistically significant effect even on the day of the event itself. Moreover, the impact of 8 of the 24 events on one-day share prices was positive, as opposed to the expected negative effect. When Dordi and Weber allow for a longer 10-day time period for measuring the impact of the various events, they then find that only 8 of the 24 total events exerted any statistically significant impact on fossil fuel share prices. That is, 16 of the 24 events – fully two-thirds of their sample – exerted no statistically significant impact within the 10-day time frame. Moreover, with the 10-day impact analysis, 11 of the 24 events exerted a positive impact on share prices.”

However it may simply be that the amount of divestment that has occurred thus far has not been sufficient for us to see the effect. I.e. the impact of any one divestment “event” (i.e. announcing a divestment) may be bigger (at the margin) if it’s happening after lots of other assets have already divested.

Working out the amount of fossil fuel assets divested thus far is not straightforward. Hansen & Pollin 2020 state that “To our knowledge, a 2016 news article by Carrington is the only published estimate of this figure. Carrington recognizes that ‘it is often difficult to calculate the precise proportion of fossil fuel investments in complex funds,’ but nevertheless reports the figure of divested fossil fuel assets to be about $400 billion as of 2016.8 However, he offers no explanation as to how he derived this figure.” And added in a footnote “In 2013, Ansar et al. provided a very wide range for an upper limit figure for the total amount of fossil fuel assets, at between $360 and $X900 billion. But they also cautioned that even this broad estimate was itself preliminary.”

Ansar et al 2013 also estimated (p40) that the total market cap of the target firms was $4,000 bn. These caveated estimates suggest divestments of around 10% of the market cap.

For comparison, it’s useful to explore the South Africa case further. Gosiger 1986 wrote that the US had $14 billion invested in South Africa, which accounted for 20% of total foreign investment in S Africa.

Various states and local authorities enacted legislation restricting public fund investment, and this mandated c$5 bn of divestment from US companies and banks involved in S Africa. 55 Universities and colleges divested $0.32bn of South Africa-related assets.

Gosiger’s analysis did not specify how the $14bn or the c$5bn split between different asset classes, however assuming these numbers seem to suggest that around one third of US assets were divested as at the time Gosiger’s paper was written (1986).

Yet in the case of South Africa too, despite what were presumably fairly substantial amounts of divestment, Teoh, Welch, and Wazzan 1999 found no statistically significant on returns.

Lastly, I note that I encountered one paper, Ewers, Donges et al (2019) (referenced in the Quigley et al divestment report), which suggested that even if only 10% - 20% of institutions divested, this could be enough to cause a crash in asset prices.

The paper does not indicate a percentage probability for the scenarios in which divestment has an effect; from reading the paper we do know that there different scenarios and in some of them divestment *does* have an effect on real world carbon emissions and in others it doesn’t.

The theory of change for this model is:

INVESTOR DIVESTS → INVESTOR SPREADS BELIEF IN FUTURE POLICY CHANGE → OTHER INVESTORS BELIEVE → PRICE SUDDENLY CRASHES

AND

OTHER INVESTORS BELIEVE → POLICY BECOMES MORE LIKELY TO BE IMPLEMENTED

The policy change in question isn’t specified in the paper, but I imagine something like an effective international carbon tax.

The model relies on a causal link whereby the policy actually becomes more likely to be implemented because of investors having more belief that the policy is coming. (equally, if investors continued to believe more and more that a strong climate policy was coming and this belief continued to grow independently of the facts, this could also lead to a similar outcome) The paper does not seem to explain why this self-fulfilling prophecy effect is justified. The authors might be imagining that if the risk of the policy change were already partly or largely priced into fossil fuel securities, it would make it easier for politicians to enact the policy changes. However I believe politicians are much more interested in job losses than stock price losses, so I don’t find this element of the model convincing.

Appendix 4: Full quantitative models for company impact?

In my ideal dream outcome for this work, the effort and energy that currently go into understanding profit are also applied to modelling externalities, both positive and negative. Those models would then be used to determine who capital is allocated, because the financial system would be internalising the externalities.

Achieving this would require overcoming a number of hurdles, many of which I see no solution for, short, perhaps, of an enormous regulatory overhaul, and probably not even then.

Having said that, if this could be achieved and done well, I believe the benefits to the world would be enormous. So I set out below some thoughts on how this modelling could be done.

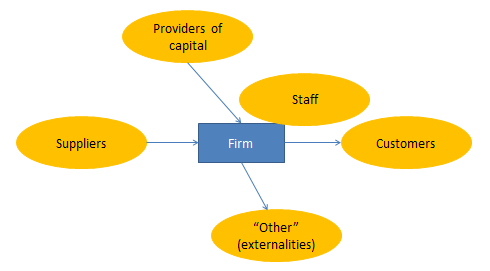

The first step is to consider stakeholders. The relevant stakeholders for a company are providers of capital, customers, staff, suppliers,, and others.

- assessing the impact on providers of capital doesn't need any further work. The finance industry already does this analysis to help decide whether to invest.

- to assess the impact of a company on its customers at first glance might seem like it needs assessing the consumer surplus. This means assessing the extent to which customers' lives are better compared to how much they pay in order to gain access to the product or service. However for a more sophisticated model we need to take into account competition. Most companies are not a monopoly. If a company which is not a monopoly ceases to exist it does not likely mean that the customer will lose out on the entirety of the customer surplus. Most likely it simply means there will be less competition i.e. the customer surplus will be reduced. Situations where the assessment of the raw consumer surplus could be important include where the consumer surplus could be negative. In principle it may seem unlikely for the consumer surplus to be negative. After all if the consumer surplus were negative why would the customer buy the product or service in the first place? However this can happen where the consumer harms are indirect or longer-term. Examples include products which could be addictive or exploitative drugs or loan sharks.

- assessing the impact of a company or its staff is a potentially lengthy and nuanced topic. However in short for companies employing people in the developed world this area is unlikely to be a cause of material harm.

- the last area is externalities. These include the environment. More broadly this could include anyone other than the stakeholders already mentioned. For example this could include people who suffer conditions from passive smoking.

Actually, this was the argument for OCC to threaten to strike down some banks’ blacklist policies against polluters last year.

Animal welfare has been an interesting case where pressure on corporations concerned with ESG policies has had some results. That’s an area where changes in antitrust law would be welcome; I think ESG regulations should make explicit reference to this area, lest regulators may proscribe some animal welfare policies as collusion.

Your post has inspired me to investigate if (and maybe later posting something about) EAs should contribute to public consultations issued by financial regulators on ESG standards to argue for explicitly inserting mentions to animal welfare. For instance, would EBA include something like this in European Banking regulations? That's why Mercy for Animals (and others) have recently asked Brazilian SEC (CVM) to mention animal welfare in regulatory norms about financial disclosures (we could provide a translation if necessary).

Curiously, I saw the idea of "universal ownership” (without this name) mentioned in this post (courtesy of Scott Alexander’s March links) about how investments are super correlated lately and how diversified investment funds have a piece of each part of the whole economy. It's the closest I've seen to computing "how much will x lose if this company drops 50%, but everyone else increases by 3%".

That would explain why BlackRock (and the financial sector, since TCFD's creation) has been so responsible lately.

Btw, could you link the Symposium you mentioned in the text relating universal ownership and fiduciary duty?

Super thanks for this post. I've seen some people arguing over this subject, yet nothing so well articulated so far. I'll post my comments remarks separately. But I'd like to begin with a very simple question:

- Is there some sort of “EA ESG Group” or “EA Financial Ethics Group”? Would it be be interesting to have it? And to link it with other groups and areas (like IIDM? Legal Topics?)?

A quick note that there's a session on it at this weekend's EA Global: Reconnect (which Sanjay is speaking at): it might catalyse formation of such a group!

Did a group form? I would love to convene one if not. For those that are interested, message me!

Those interested in this path might enjoy interviews with Lauren Taylor Wolfe — and reading about the work of Québec's pension plan, John Kerry and Mark Gallogly, and Mark Carney to drive more effective ESG investing and governance norms.