You’ve probably seen the Nancy Pelosi Stock Tracker on X or else a collection of articles and books exposing the secret and lucrative world of congressional insider trading.

The underlying claim behind these stories is intuitive and compelling. Regulations, taxes, and subsidies can make or break entire industries and congresspeople can get information on these rules before anyone else, so it wouldn’t be surprising if they used this information to make profitable stock trades.

But do congresspeople really have a consistent advantage over the market? Or is this narrative built on a cherrypicked selection of a few good years for a few lucky traders?

Is Congressional Insider Trading Real

There are several papers in economics and finance on this topic

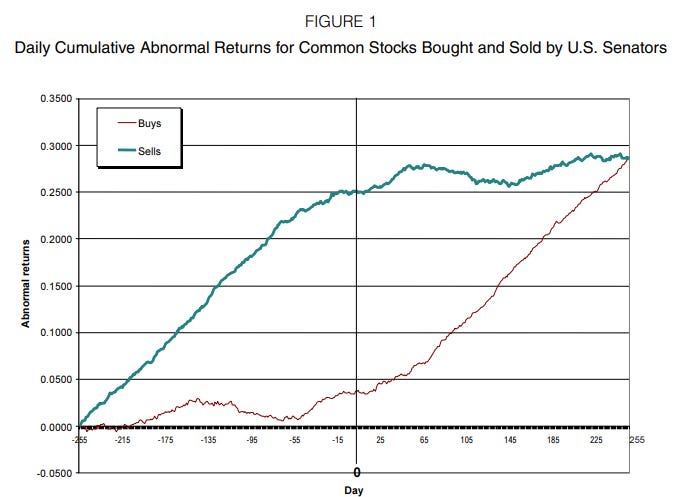

First is the 2004 paper: Abnormal Returns from the Common Stock Investments of the U.S. Senate by Ziobrowski et al. They look at Senator’s stock transactions over 1993-1998 and construct a synthetic portfolio based on those transactions to measure their performance.

This is the headline graph. The red line tracks the portfolio of stocks that Senators bought, and the blue line the portfolio that Senators sold. Each day, the performance of these portfolios is compared to the market index and the cumulative difference between them is plotted on the graph. The synthetic portfolios start at day -255, a year (of trading days) before any transactions happen.

In the year leading up to day 0, the stocks that Senators will buy (red line) basically just tracks the market index. On some days, the daily return from the Senator’s buy portfolio outperforms the index and the line moves up, on others it underperforms and the line moves down. Cumulatively over the whole year, you don’t gain much over the index.

The stocks that Senators will sell (blue line), on the other hand, rapidly and consistently outperform the market index in the year leading up to the Senator’s transaction.

After the Senator buys the red portfolio and sells the blue portfolio, the trends reverse. The Senator’s transactions seem incredibly prescient. Right after they buy the red stocks, that portfolio goes on a tear, running up the index by 25% over the next year. They also pick the right time to sell the blue portfolio, as it barely gains over the index over the year after they sell.

Ziobrowski finds that the buy portfolio of the average senator, weighted by their trading volume, earns a compounded annual rate of return of 31.1% compared to the market index which earns only 21.3% a year over this period 1993-1998.

This definitely seems like evidence of incredibly well timed trades and above-market performance. There are a couple of caveats and details to keep in mind though.

First, it’s only a 5-year period. Additionally, any transactions from a senator in a given year a pretty rare:

Only a minority of Senators buy individual common stocks, never more than 38% in any one year.

So sample sizes are pretty low in the noisy and highly skewed distribution of stock market returns.

Another problem, the data on transactions isn’t that precise.

Senators report the dollar volume of transactions only within broad ranges ($1,001 to $15,000, $15,001 to $50,000, $50,001 to $100,000, $100,001 to $250,000, $250,001 to $500,000, $500,001 to $1,000,000 and over $1,000,000)

These ranges are wide and the largest trades are top-coded.

Finally, there are some pieces of the story that don’t neatly fit in to an insider trading narrative. For example:

The common stock investments of Senators with the least seniority (serving less than seven years) outperform the investments of the most senior Senators (serving more than 16 years) by a statistically significant margin.

Still though, several other papers corroborate the claim that congresspeople consistently beat market returns. And it doesn’t seem like this is just selection effects where being a good trader helps you get elected. Congresspeople also have to report their transactions when they are campaigning, before they get into congress and any powerful committees. Fresh congress members don’t beat the market.

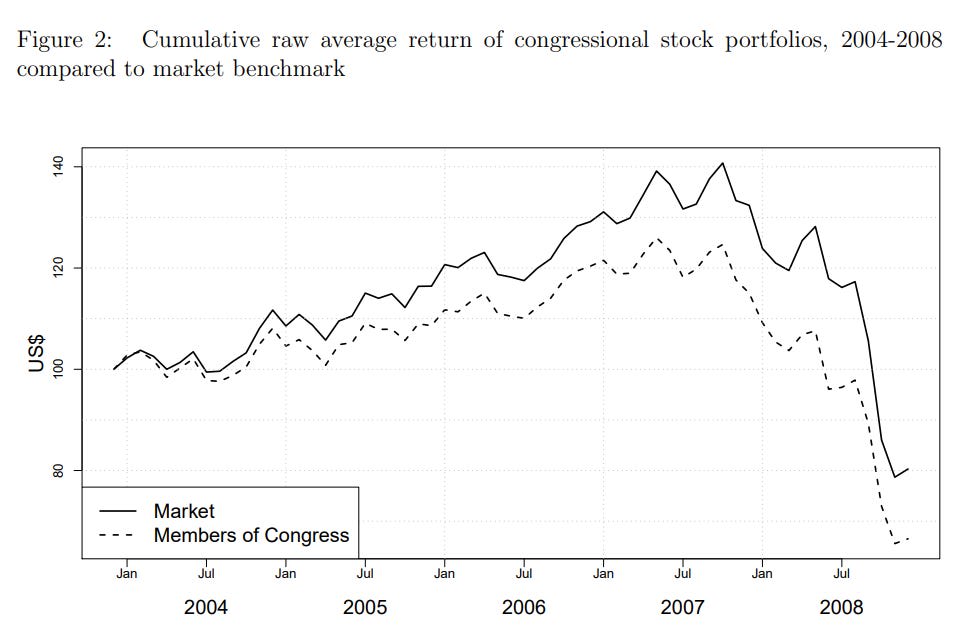

These papers don’t settle the issue though. Andrew Eggers and Jens Hainmueller from LSE and MIT claim that Ziobrowski’s research is weak. The results from the above paper aren’t reliable measures of above-market returns for two main reasons.

One is their synthetic portfolio approach. Ziobrowski tracked the stocks that Senators bought or sold, and then built a portfolio which held the stocks senators will sell for a year prior and held the stocks that senators buy for a year after, but this does not reflect what Senators actually did with their portfolio. Also, a large majority of most Senator’s stock portfolio is not bought or sold in any given year, so the synthetic approach can only give a noisy estimate of a small slice of their actual portfolio.

The other problem is that Ziobrowski’s results are very sensitive to choices about how to weight and aggregate the transactions of Senators. Only a minority of Senators trade stocks and among those that do, just a couple big traders and big trades dominate the rest in size. Ziobrowski only gets a statistically significant estimate of Senator’s advantage over the market when they look at the aggregate trade-weighted portfolio of all senators, which puts a ton of weight on a few big trades from a few members. In all other specifications, like weighting the returns for each senator equally, the estimated advantage over the market isn’t distinguishable from random noise, though the point estimates are still positive and large.

Eggers and Hainmueller run their own regression or more detailed financial disclosure data from 2004-2008 that allows them to actually construct congressional portfolios without assuming a 12-month holding period for each transaction. They find that the average congressional portfolio underperformed the market by 2-3%.

The aggregate trade-weighted portfolio of congresspeople does better, as in Ziobrowski, but only matches the market.

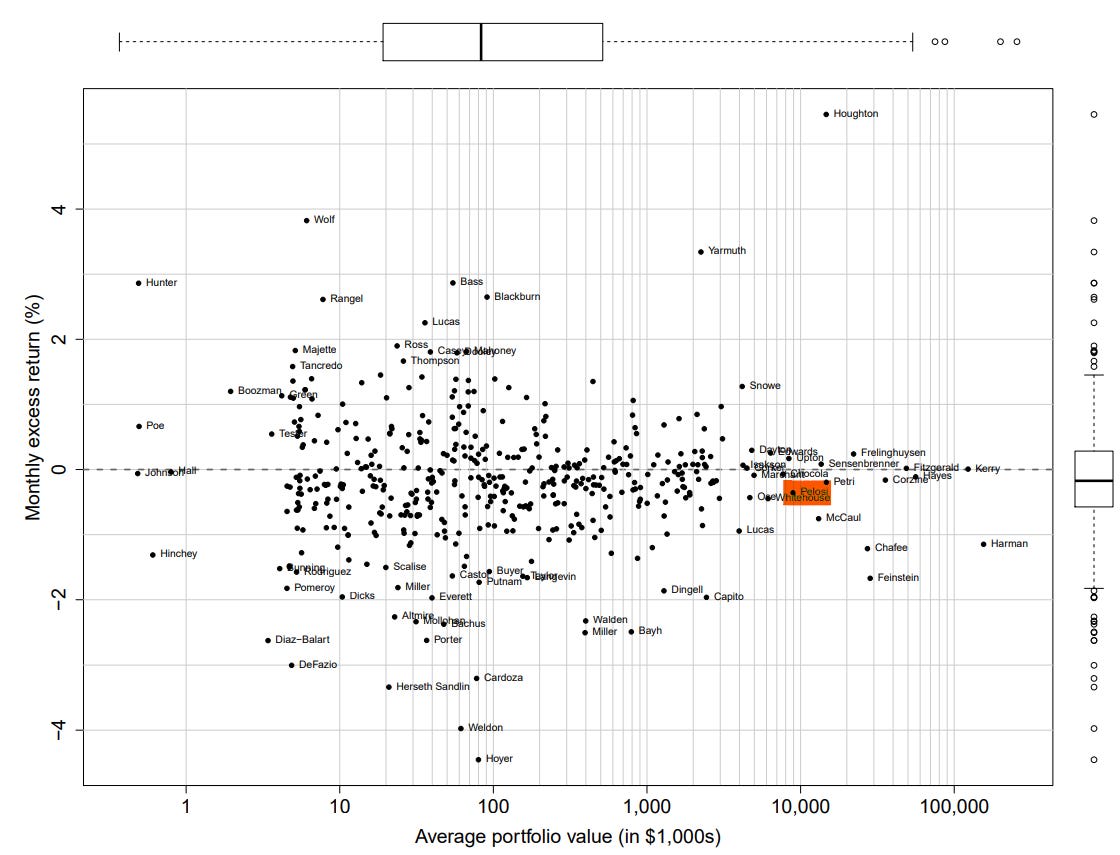

Eggers and Hainmueller also have this plot of each member’s portfolio performance compared to the market index (y-axis) vs the portfolio’s size (x-axis). There are lots of congresspeople who beat the market, but slightly more who don’t, so the median congressperson slightly underperforms the index. Even Nancy Pelosi (highlighted in red) underperforms the market over this period.

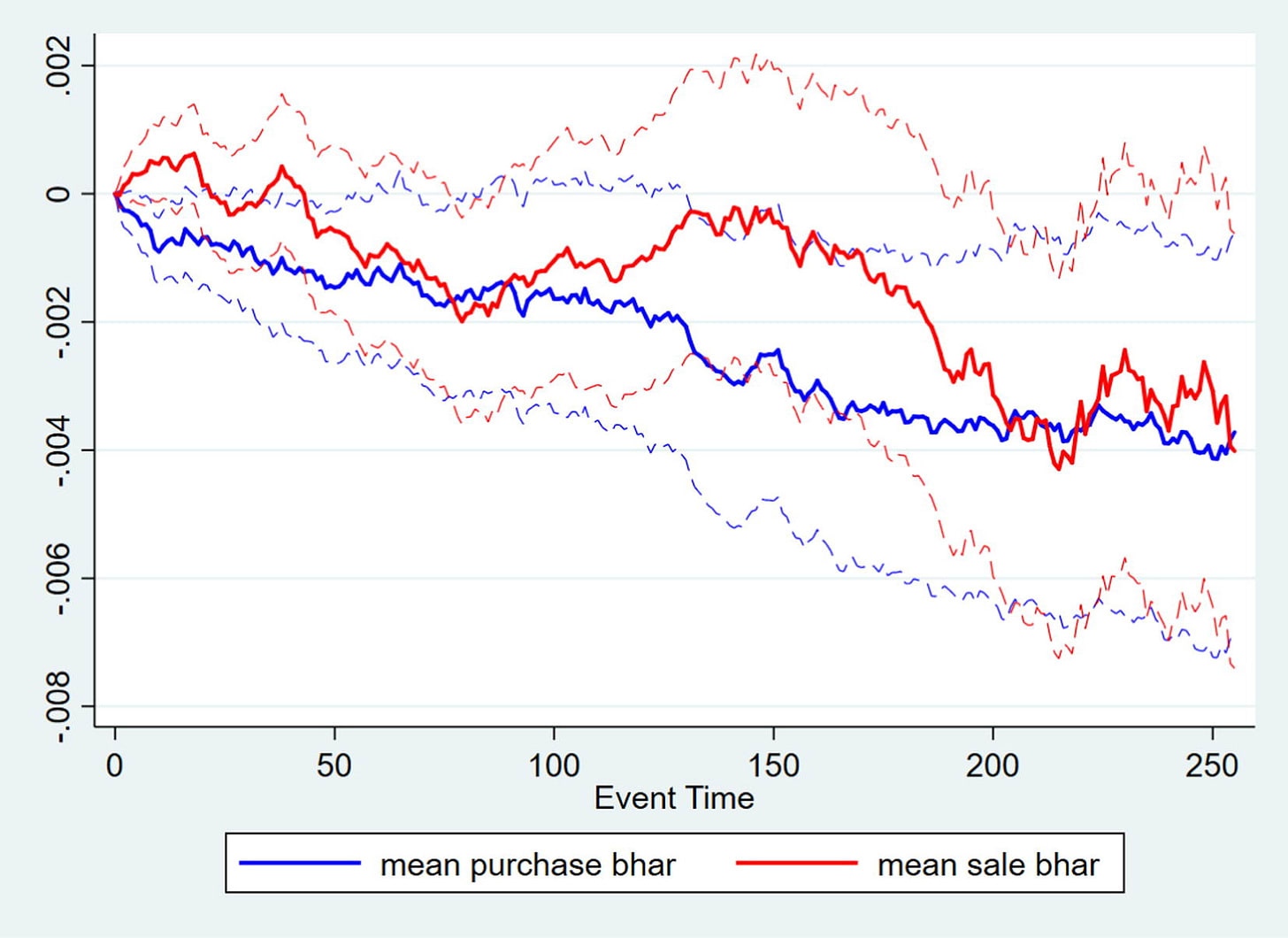

Bruce Sacerdote of Dartmouth also investigates congressional stock trading and similarly finds no evidence of outperformance over 2012-2020. They replicate a graph similar to Ziobrowski’s stock timing chart I showed at the top where here the red line tracks the price performance of stocks that congresspeople sold compared to an index* and the blue line does the same for stocks they bought.

The modern member’s sell portfolio slightly underperforms the index, which is what an savvy senator would want, but this is barely distinguishable from noise and probably not enough to profit off of after transactions costs. The stocks that congresspeople buy underperform the market by a similar amount, definitely not what an informed insider would want.

*the index that these lines are compared to isn’t a total market index as in Ziobrowski, but an index for the industry that the stock is in. They also look at comparing to the total market index and find the same results but they don’t graph them.

What about Pelosi in particular? As we saw above, there are long periods where she underperforms the market, even during the financial crisis when congress is playing a larger part than usual in the economy. Out of hundreds of congresspeople, one beating the market enough times for lots of articles to be written about it is expected. If all members of congress flipped a coin 10 times, Pelosi might get ten heads in a row.

You can see her financial disclosures here. Here’s an example from 2023

Overall, I read this literature as being consistent with basically par-market performance among congresspeople with lots of noise and probably a few big insider trades that really do benefit from private information. This lack of insider trading is in part due to lack of actually useful and unique information, but is also a result of the existing political and legal constraints on congresspeople which push many of them away from the stock market all together.

Can we use Congressional Insider Trading to our Advantage?

Congressional stock trading should probably be banned. Free reign on trading allows politicians to personally enrich themselves while tanking everyone else. Shorting Meta before sending the FTC to break them up, for example, or going long on Zoom as you shut down travel in 2020.

However, we shouldn’t completely separate congresspeople from the stock market. A fixed salary might avoid negative correlation between the country doing well and their personal wealth; they get paid the same whether the economy is on fire or down in flames, but we can do better than uncorrelated.

Ban stock trading for politicians but tie all of their salaries to an aggregate index of the US economy. All political salaries should be paid as 10-year locked shares of the total market index. If politicians have outside wealth coming in, they can invest it, but only in this long-term index. This has two advantages.

One, is that it’s just a flexible and populist-compatible way of increasing politician’s salaries. High politician salaries are seen as a form of corruption, and they often are in countries with underdeveloped and extractive institutions. But in stable democracies with solid rule of law, talent is a more important constraint than corruption. Singapore has the best civil servants in the world in large part because they peg their salaries to be competitive with the private sector. Congressional salaries haven’t risen in nominal terms since 2009, which means they have shrunk massively in real terms. As this shrinks more, it gets harder for people without independent wealth or outside support to afford the office and harder to attract top talent into civil service.

{kind=link}

Raising their own salaries is politically ugly, but pegging them to an index is a flexible way to keep salaries high as time goes on while also being obfuscated enough to avoid populist ire.

The second advantage is incentive alignment. Insider trading is bad because it allows congresspeople to profit off of changes that hurt the aggregate wealth of the nation. Fixed salaries with no trading are an improvement on this, but we can do better. Index fund salaries are commission payments on broad-based economic growth. Big corporations incentivize their employees with stock options, we should incentivize government employees with stock options on the nation as a whole.

Big corporations also generally put a time lock on stock options to incentivize commitment, and we should do the same here. 10-year locked index shares couldn’t be sold or traded for a decade, but congress members can fund their current expenses with loans taken out on the future value. This longer-term lock disincentivizes congresspeople from colluding on short-term pump-and-dumps e.g by funneling subsidies into the stock market for short term gains.

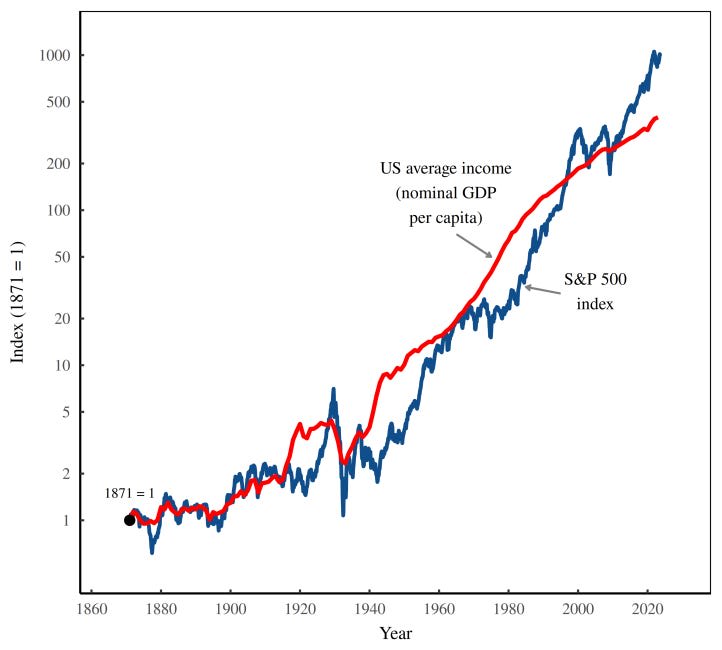

Index funds are a reasonably good correlate of important welfare metrics like GDP per capita, especially over the long term.

Though they are much noisier. As an alternative, one could also pay congresspeople a fixed multiple of GDP per capita which would have the same benefits without the volatility.

Whether or not Nancy Pelosi is making millions off of her congressional information network, we could still do a lot to align her incentives with our own. Attaching her net worth to an index of future economic growth would put our interests front-and-center in her own personal welfare maximization.

Congressional insider trading is probably not a massive problem nor a consistent source of wealth for most members of congress. It’s probably worth diminishing the practice even more, but we shouldn’t stop there. The problems of congressional insider trading imply the potential of congressional stock options.

Paying politicians high salaries which rely on positive expectations for future economic growth simultaneously attracts better talent to the job and ensures that they want to grow the economy as much as the rest of us.