Cain Hillier

Bio

Participation1

I'm currently an undergraduate study at the University of Sydney and a Technical Writer for Schneider Electric. Later in the year, I'll be undertaking an MPhil in Global Risk and Resilience at CSER.

Posts 1

Comments3

I didn't articulate myself clearly enough — first-time poster blues! I'd argue these co-builds are a destabilising force for the same reason I mentioned Pine Gap (without explaining myself, whoops).

The benefits allies receive from these facilities are often at the expense of sovereignty over the site or technical oversight by local regulatory bodies.

Now, this tradeoff might be worth it for the intelligence agencies, but the US presence is often conspicuous and jarring to the local population, even in a remote area like Alice Springs, where PG is located. It would be especially so in a major metropolitan area like Sydney, Melbourne, or Canberra, where these DCs would likely be built.

Given the lack of trust foreign populations currently have for the US as a security partner, it would be political anathema for most WEIRD nations, at least within the next four years, to announce these types of co-builds.

There's also a question of what incentives the US would have to create these co-builds if they do provide this spying capability to allies, given the disproportionate amount of local compute to draw upon, particularly in Northern Virginia near the existing Washington security apparatus.

Re: your excellent last point, how might this leverage be exercised in a way that leads to greater stability? What type of capital is created? Where would it be expended and to what ends?

In short, I'm very sceptical these co-builds will happen. If they did, they'd be a political football of national relevance in nearly all allies. I'm unsure how allies would use them to cultivate stability, as I'm unsure what criteria we're judging stability by.

Thanks for getting me to explain myself a bit better!

Hey Caleb,

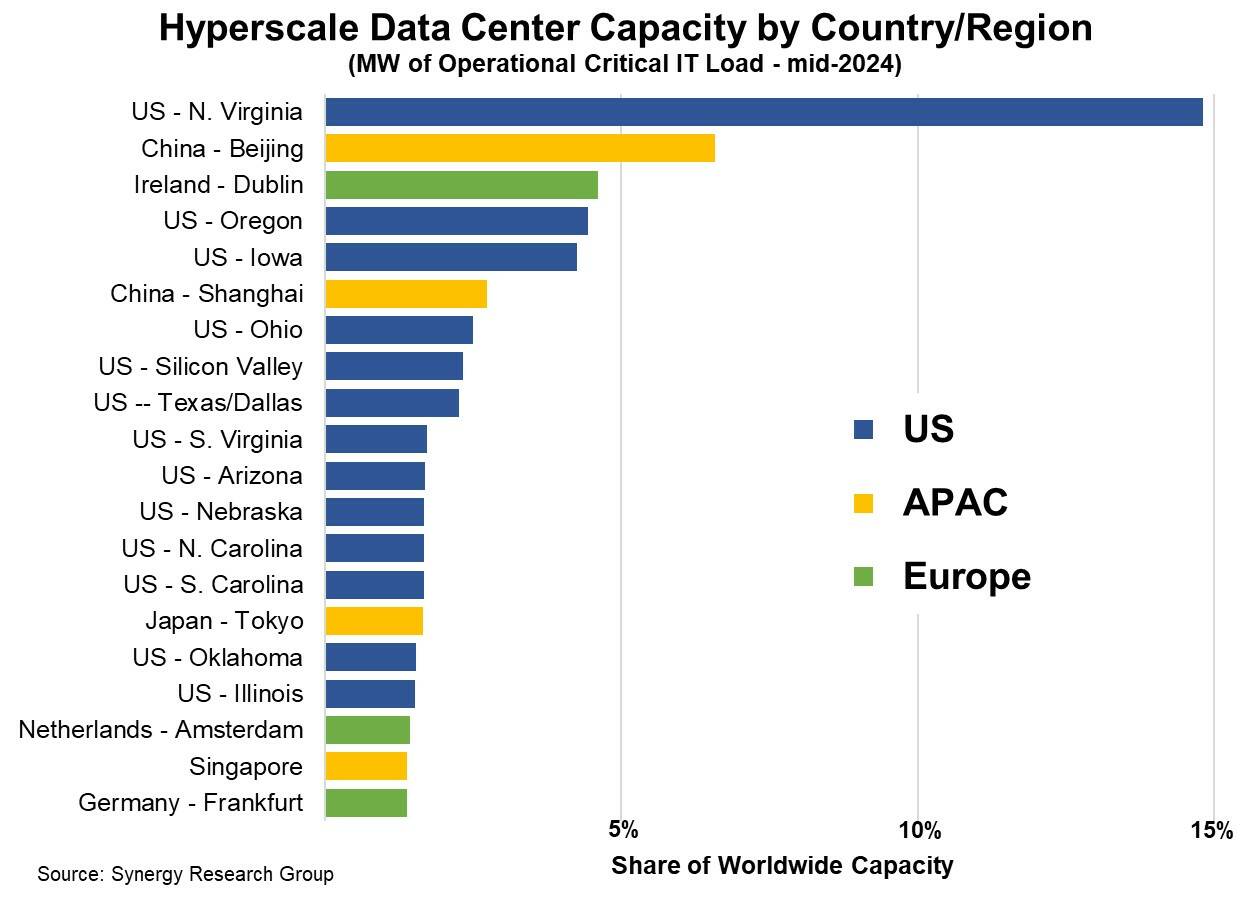

For the first take, I'd say the answer is likely geopolitically destabilising. I work in the DC infrastructure industry for a US ally, and we're seeing a deluge of sovereign GPU cloud providers popping up with bare metal, locally housed solutions for defence/gov contracts. There's a market bet (at least in Australia) that compliance demands will favour local AI IaaS providers over co-builds, even if US-operated hyperscalers might provide far greater functionality across the stack. Another valuable reference point would be the political controversy regarding Pine Gap, a joint communications and signals base between the US and Australia.

Re: Point 5. I strongly agree; this is likely to be my research focus during my upcoming MPhil at CSER. While many provider to consumer deployment pathways are currently governed by convention, there are possible regulatory paths to influence key process owners in digital infrastructure to take greater autonomy over their roles and veto risky deployments.

The recent rise of AI Factory/Neocloud companies like CoreWeave, Lambda and Crusoe strikes me as feverish and financially unsound. These companies are highly overleveraged, offering GPU access as a commodity to a monopsony. Spending vast amounts of capex on a product that must be highly substitutive to compete with hyperscalers on cost strikes me as an unsustainable business model in the long term. The association of these companies with the 'AI Boom' could cause collateral reputation damage to more reputable firms if these Neoclouds go belly up.

And, if you're in a race-to-the-bottom price war on margins, fewer resources are devoted to risk management and considerate deployment. A recent SemiAnalysis article confirms the "long tail" of these companies that lack even basic ISO27001 or SOC 2 certs.

I should say that the Sovereign Neocloud model seems to alleviate both the financial and x-risk concerns; however, that's mostly relevant outside the US and China.