I became the CEO of EV US in January 2023. I worked alongside the EV US and UK teams, former EV UK CEO Howie Lempel, and current EV UK CEO Rob Gledhill to recover and reform Effective Ventures and improve the robustness of the EA ecosystem in the aftermath of FTX’s collapse. Amidst these efforts, I and others learned or fortified lessons that I think aren’t unique to EV and could be valuable to the wider EA community. Being able to look at hard problems, discuss them with candor, and update based on what we learn are values that I admire, and I see them as a positive and necessary mechanism for doing good. I want to act on those values here.

Goals of this post

- Provide an update to create communal knowledge: Clarify what reforms have taken place at EV in recent years and the reasoning behind them.

- Offer potential lessons: Document both institutional changes and the fuzzier lessons learned, and provide a cultural nudge to take governance and operations more seriously.

- Honor commitments: Make good on prior commitments to “share additional reflections when they’re ready.”

The views in this post are my own. I don’t represent or speak on behalf of my current or former colleagues at EV US or UK, or from my current role as CEO of CEA, or on behalf of the EV US or EV UK boards. While I did seek input from others to help write and fact-check this post, I would expect differences of perspective and that reasonable people might disagree about the history or lessons learned.

Some high-level notes on FTX-related reflection

Before I get into the rest of the post, I think it’s important to note that a number of issues have made it harder for the EA community to have a group conversation, process what happened with FTX, take decisive action, and get back on track. For instance:

- Many people who had access to certain kinds of private information haven’t been communicating publicly very much. I understand why — and I’m one of these people, which I’ll discuss more in the post, including in the section on EV’s comms policy. But unfortunately, this has made it hard for the EA community to get a sense for what happened and has probably caused some people to feel like they’re being ignored or dismissed, that their concerns aren’t being taken seriously, or like information is being deliberately hidden.

- It’s often unclear who actually holds the ball for clarifying what happened or taking accountability for some failures in EA. This is because some mistakes were made by omission or because responsibility for collective decisions was diffused across many people, which can make it feel no one is “stepping up” and owning these issues. This lack of clarity was, in part, because there wasn’t a clear individual holding the ball. Additionally, once potential individuals were in place (e.g., the CEOs of EV US and EV UK), their attention was divided by many urgent responsibilities such that it was difficult to find the bandwidth for public communications.

- It’s hard to clearly acknowledge the harm people in the EA community have experienced while still distinguishing “mistakes” from “reasonable decisions that had serious costs” (which I think is important for understanding what happened and why). I think many conversations have struggled to do both.

All of this can mean that some basic but important points tend to get lost or left unstated. So, I want to explicitly say:

- I believe EV made mistakes that negatively affected the community. To be clear, the independent investigation by Mintz found no evidence that anyone at EV knew about the alleged fraudulent criminal conduct at FTX and Alameda. But there are many types of mistakes that fall short of (complicity in) criminal activity. I discuss some things that I think are mistakes in this post.

- I also believe EV did many things right. Even amidst the FTX-induced crisis, I spoke with project leaders who reaffirmed that joining EV was a good choice for their organization, and other external organizations continued to ask if they could join EV. I am very grateful to the many people who poured significant amounts of time and effort into enabling EV to do the good it has accomplished, both before and after the crisis. Moreover, I don’t want someone to think that I’m arguing for something like “never set up a fiscal sponsor” — I think it can be good, but it should be done correctly.

- I think many (though not all) complicated decisions EV made in the aftermath of the FTX collapse had real costs for the EA community, but were ultimately good decisions. I discuss some of the trade-offs faced in more detail below.

I value people in the EA community and want to invest in the EA community’s health. Sometimes I (and EV and CEA) will need to make choices that require a trade-off between the community’s desires and the betterment of the world as a whole, and I endorse making those trade-offs when they occur.[1] At the same time, much of the impact I expect CEA to have is by helping the community flourish in its pursuit of our shared goals. I also want to acknowledge how stressful and challenging the past couple of years have been for many people involved in EA. I know that some people have felt confused, abandoned, or betrayed by some leaders and institutions in EA. I want to do what I can to improve the situation. To be an effective collaborator with the community and build shared trust, I think it’s worth communicating extra context around areas of concern when possible.

The EA Forum is also a channel that I hope to use more to share updates with the EA community. At the same time, I want to flag that given limits to my bandwidth, I will probably not be commenting very much.

Scope of this post

I’m focusing on the following:

- The actions Effective Ventures has taken: This is not an all-encompassing answer to how people changed their beliefs in the fallout of the FTX collapse or what lessons have been learned related to FTX. You can find FTX reflections from various prominent people in the EA community in the Appendix.

- Reforms the UK Charity Commission referenced: When Howie Lempel (then CEO of EV UK) shared that the Charity Commission for England and Wales had announced a statutory inquiry into EV UK, some people were understandably concerned and raised questions about the governance and operations of EV.

- The Charity Commission has since released its report (you can read their press release on it here and EV UK’s Forum post about the conclusion). The Commission noted that no major issues arose in practice but referenced some areas where EV’s processes were suboptimal and noted that “both the finance and legal teams at the charity have been strengthened and policies have been bolstered or created with more robust frameworks.” I wanted to share more about these changes.

- Note that we didn’t actually enact any reforms because of recommendations from the Charity Commission. All of the reforms the Commission referenced happened proactively.

- Lessons learned: Many of the lessons were painful and required significant amounts of time, money, and stress to address. My hope is that the community as a whole can learn from the work of EV’s team without future organizations needing to experience similar turmoil firsthand. In particular, I think the information in this post can be useful for other organizations looking to establish or improve their governance and operations.

- The role of organizations like EV in the EA ecosystem and how they could function in the future: I have heard demand from others in the EA ecosystem for an organization to serve a function similar to EV (e.g. fiscal sponsorship and/or operational support). While I feel strongly that EV was not in a good position to serve that role, I think it’s possible other organizations could be created to fill this vacuum, and I want to provide information that could help others succeed. Importantly, I think many valuable improvements have occurred that others can learn from. I also think this post highlights ways in which EV still falls short of an optimal organization. I think it would be bad if someone attempted to copy and paste EV’s practices to another organization.

What’s not in scope:

- Broader cultural lessons for the EA community related to FTX. This post focuses on institutional reforms instead of broader cultural lessons for the community. While I think those lessons are important, writing a post like this takes an immense amount of time and I didn’t want to delay it further. Moreover, others have shared reflections related to the broader community (some of which are included in the Appendix).

- Information where sharing it would have significant downsides, e.g. information with legal constraints, information received on the condition of confidentiality, or sensitive information about personnel. Sometimes we may share information of this type if there are important reasons for it to be public, but in general we have a high bar for doing so.

Additional notes on this post and how to read it:

- Not all of the reforms or actions discussed here were directly caused by FTX. Some actions were a direct response to problems exposed by the FTX crisis, such as improving donor due diligence. But some actions were only indirectly caused by the FTX crisis. FTX and the resulting internal and external scrutiny served as a prompt for us to step back and examine EV’s strategic and operational practices. Many of these reforms would have been wise even before the FTX crisis, like hiring CEOs. Some reforms were also the result of non-FTX issues or a mix of different issues coming together. An example of a policy change that happened independently of FTX includes updates to the sexual misconduct policy, which were prompted by EV’s investigation into reports of sexual misconduct by a board member.

- Throughout the post, “I” refers to Zach Robinson, and I sometimes use “we” to describe institutional changes made at EV. “We” is thus a particularly blurry term, as sometimes I was heavily involved, and at other times action was taken without significant involvement from me, e.g. because they occurred before I joined in early 2023 or because there was an intentional division of labor between me and someone else like Howie (who was leading EV UK). Even when I use “I”, I want to communicate my limited perspective but certainly don’t want to claim sole credit for reforms. Most importantly, while I am grateful for the work that others have put into both the reforms and reviewing this post, I do not claim this post represents a consensus view between EV staff, leadership, or board members.

- Throughout the post, “EV” refers to both EV UK and EV US, which are two independent entities that collaborate closely due to a shared mission and purpose. In this post, I use EV when referring to the actions taken and agreed upon by both EV US and EV UK (see Background on EV). It is in these areas of policies and controls, as highlighted in this post, where the two entities worked especially closely to improve governance for both EV US and EV UK.

- This post is long, and I don’t expect the average Forum user to read the whole post. Some may want to skim the summary and background, and click through to learn about the reforms and actions or lessons that are most interesting to them.

Summary of reforms and actions taken at EV

- Hiring CEOs (and other non-board personnel) for EV US and EV UK: EV hired CEOs of EV US and EV UK to add more executive capacity and speed up decision-making, while also hiring other staff members who brought valuable expertise to help reform EV (e.g. lawyers).

- Changes to EV US and EV UK boards: Both the EV US and EV UK boards have seen 100% turnover since the FTX collapse. Changes to the boards occurred for multiple reasons discussed below.

- FTX-related investigations: An independent investigation found no evidence that anyone at EV was aware of the criminal fraud of which Sam Bankman-Fried has now been convicted. We don’t currently plan to conduct any further investigations.

- Instituting financial reforms: We instituted better financial controls, improved our financial auditing, and scaled up our finance team to include people with more finance experience.

- Improving donor due diligence: We formalized a donor due diligence process that requires checking the background of all people who donate or seem likely to donate above a certain threshold to EV or its individual projects.

- Adopting a restrictive communications policy: In the immediate aftermath of the FTX crash, EV temporarily adopted a communications policy that restricted staff and board members' external communication, based on strong internal and external legal advice. This policy loosened over time.

- Streamlining whistleblowing policies: EV updated its whistleblowing policies to better protect whistleblowers and reduce the fear or friction that could stop people from speaking up.

- Updating anti-harassment and misconduct policies: We updated EV’s anti-harassment and misconduct policies to add more points of contact, clarify situations in which things would be escalated, and make anonymous submission easier. This was the result of allegations of sexual misconduct against a former EV UK board member.

- Improving the COI policy: EV formalized conflict of interest reporting for board members and the CEOs of EV US and EV UK, as well as processes to make it more likely these are kept up to date.

- Clarifying the level of separation between the EV US and EV UK entities: The boards clarified the level of independence between EV US and EV UK, while the two charities kept working closely together.

- Initiating EV shut down: The EV US and EV UK boards decided to spin out all of EV’s projects over the coming months and years and will not be replacing them with new sponsored projects.

Background on EV

Effective Ventures Foundation (“EV”) refers to two separate legal entities, each with their own CEO and boards:

- Effective Ventures Foundation in the UK (“EV UK”)

- Effective Ventures Foundation USA in the US (“EV US”)

What we now call Effective Ventures was created in 2011 as an umbrella entity for the fledgling 80,000 Hours and Giving What We Can projects, and was originally called the Centre for Effective Altruism (which is not the same as present day CEA, which is a project within EV).[2] Then-CEA, now-EV, played an important role in the growth of the EA ecosystem. EV eventually became a fiscal sponsor and enabled projects to launch with lower friction than they would have otherwise. Projects were also able to take advantage of economies of scale by centralizing operations. By November 2022, EV had grown to legally sponsor and help operate the following projects (some of which are now their own independent entities):

- 80,000 Hours

- Asterisk

- BlueDot Impact

- Centre for Effective Altruism

- Centre for the Governance of AI

- EA Funds

- Forethought Foundation

- Giving What We Can

- Longview Philanthropy

- Non-Trivial

- Wytham Abbey

- Three individuals doing independent research

(Yes, this is extremely confusing.)

EV’s operational and oversight capacity didn’t keep up with this growth. The governance and operational systems EV originally put in place were set up to support a much smaller organization that housed fewer projects and had significantly fewer financial resources. These systems were not adequately updated when EV rapidly scaled to house around a dozen projects and tens of millions more dollars. As a result, EV had internal governance issues and EV as a legal entity was poorly set up to handle the fallout from crises.

For example, in mid 2022, there was only one in-house lawyer. She had just started in July 2022 (just a few months before the FTX collapse), covered all projects that operated in the UK , and had no full-time equivalent at EV US to manage EV US legal issues. As another example, EV board members spent more time on EV-related duties than board members spend on a typical non-profit, but because their efforts were divided between many independent projects the time per project remained too low to provide optimal oversight. There also weren’t policies in place for what would happen if one project took actions that risked the wellbeing of other projects, e.g. by taking inappropriate risks, attracting negative PR, or running out of funding.

To the boards’ credit, my understanding is that they had begun to discuss reforms before the FTX collapse. However, for the most part they did not take significant steps to implement these reforms until after. The FTX collapse directly and indirectly triggered many serious challenges and exposed underlying problems that stemmed from a lack of sufficient executive capacity and oversight within EV US and UK relative to its legal, financial, and operational importance in the EA ecosystem.

After a year of instituting reforms for all organizations under the EV umbrella, which the rest of the post discusses, the boards of EV US and EV UK decided to wind down their respective umbrella orgs and spin out the various projects. Several of the projects under the Effective Ventures umbrella have already completed spinning out as individual nonprofits, and the remainder are in the process of doing so.

You can read more about EV’s structure here.

Reforms and other actions taken

Hiring CEOs (and other non-board personnel) for EV US and EV UK

Background context

Prior to the collapse of FTX, EV US and EV UK did not have CEOs or executive teams tasked with holistic responsibility for EV. The decision-making process for the organizations relied on board decisions.

What actions were taken and why

The FTX collapse prompted EV to notice how much it needed to mature. In particular, we needed CEOs and chief of staff-type roles: people who worked on EV full-time and were empowered to make cross-entity decisions faster than a board or other committee could. Moreover, these individuals would feel a more direct sense of responsibility for EV’s outcomes compared to a broader set of volunteer board members.

Howie Lempel was hired as the Interim CEO of EV UK in November 2022 and I was hired as the Interim CEO of EV US in January 2023. As the announcement post on this said at the time, “It’s not ideal to have boards playing the role of executives, so the boards have now also appointed Interim CEOs to each charity.” More recently, Rob Gledhill replaced Howie Lempel as CEO of EV UK, while I remain CEO of EV US, but with intentionally reduced capacity. I have handed off many responsibilities to Rob while I focus primarily on CEA.

We also hired and made changes to the EV operations, finance, and legal teams. Related to finance, we needed people with more experience leading the team, especially given the more complicated situation EV was in after the FTX collapse (as noted in the recent report from the Charity Commission). Similarly, we needed further legal capacity and advice, so we hired a full-time legal team.

Culture change was also important, and one of the best ways to change culture is to change people. This is particularly true for senior staff. By bringing in CEOs and other staff with a specific mandate to improve compliance and professionalization, we both introduced decision-makers without emotional ties to the status quo and sent a signal to existing staff about the importance of these new priorities.

Ongoing considerations

We would ideally have separate CEOs of EV US and CEA, both for time allocation reasons and conflict-of-interest (COI) mitigation. Ideally, I would have been replaced in my role as CEO of EV US; but after a long hiring process, the EV executive team and US board couldn’t find a candidate who had the same level of context regarding complex tradeoffs (including idiosyncratic ones specific to the EA community) and operations experience that the role requires. (Similarly, CEA’s incoming COO, Anna Weldon, has served on the EV US board and has context on the work that will be hard to replace.) Since CEA has yet to spin out of EV, though, in many ways CEA and EV’s interests converge; CEA is affected by issues that affect all of EV. If and when there are COIs, I disclose those to the board and will be recused when appropriate (for example related to CEA’s future spinout).

The difficulty in finding a suitable CEO replacement gestures at a broader point that it can be extremely challenging to attract excellent CEOs and board members. Consider:

- There is no job security for full-time staff as EV is shutting down.

- EV board roles are unusually time consuming (as discussed below).

- These roles are highly visible and can be subject to public criticism that gets magnified on the Forum (though I’ve found people to be overwhelmingly kind and appreciative in private).

- I think Holly Elmore does an excellent job discussing some of the downsides of criticism here.

- It can be difficult to respond to such criticism due to the confidential nature of the information driving many decisions.

- It can be challenging for candidates to know what they are getting themselves into when they don’t have access to legally privileged information (this was particularly challenging prior to the FTX settlement).

- Many senior decision makers have found these roles immensely stressful and emotionally draining.

I hesitated to include the content above, as I don’t intend for this to read as a “woe is me” list. I’m happy I took the job! But I also think I’m unusually emotionally resilient and that my experience wouldn’t generalize to most others. Moreover, I believe there’s an important point to be made about EA culture. In particular, I think it would be highly valuable to figure out how to better celebrate people who contribute to the community by stepping up into leadership positions out of a sense of altruism and how to combine that with constructive criticism so that it becomes less of a deterrent to people taking on leadership roles. I think these cultural changes would make it easier for EA organizations to attract strong candidates for important positions.[3]

Changes to EV US and EV UK board

Background context

As two distinct legal entities operating in different countries, EV US and EV UK each have had their own individual board since their creation. The responsibilities of a charity or non-profit board in both the US and the UK broadly include governing and overseeing the organization’s activities, which can include responsibilities like ensuring legal compliance, strategic planning, and fiduciary duties. Especially prior to the hiring of CEOs of EV US and UK, the boards served as major decision-makers for the charities.

It can be difficult and somewhat misleading to view boards as unified entities; there are many different individual decision-makers on each board. When we say one of the boards made a decision or took an action, readers shouldn't assume that everyone on that board reached the same conclusion or had the same reasons for what they did.

What actions were taken and why

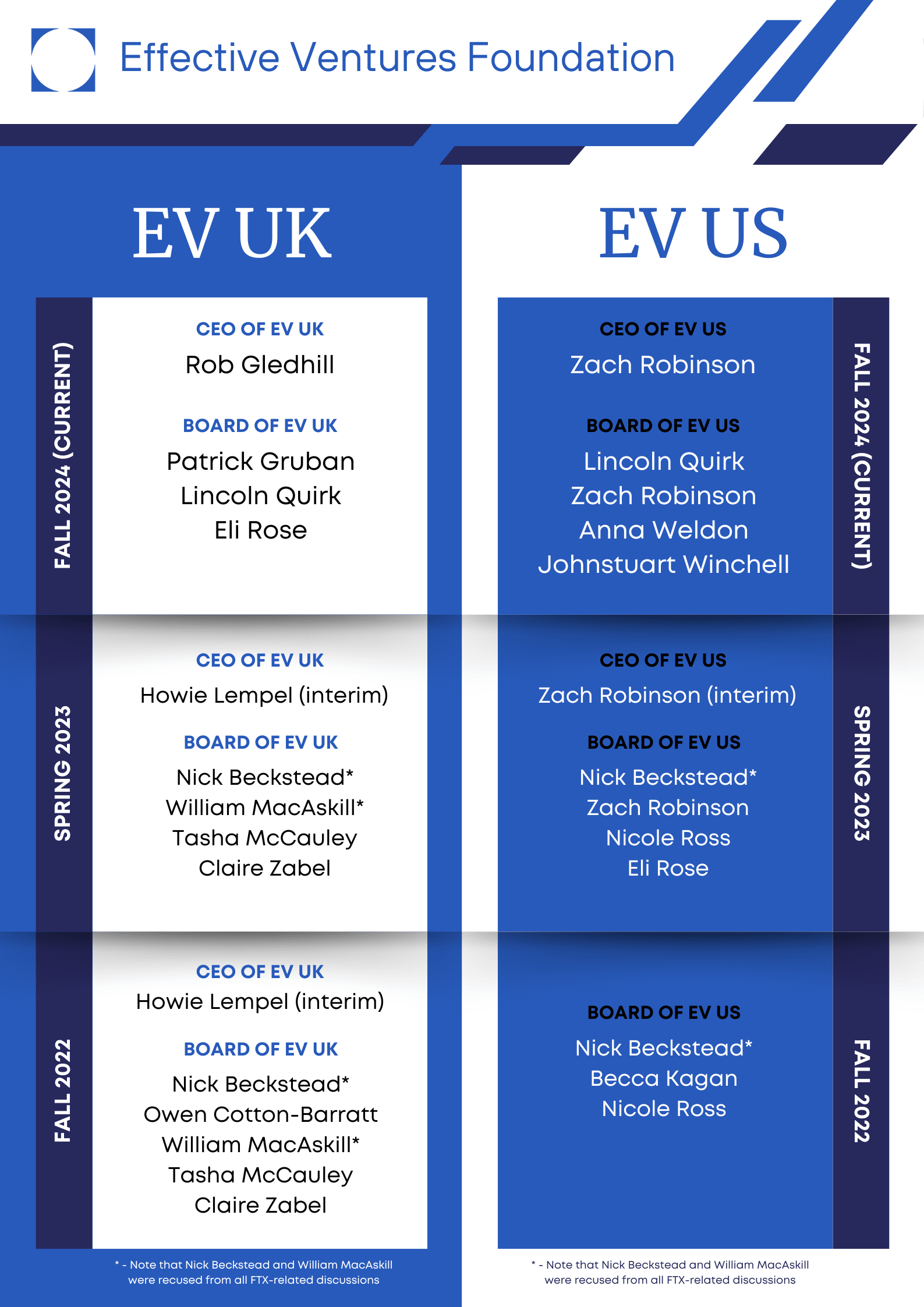

Both the EV US and EV UK boards have had complete turnover in the past few years, as represented below:

Different changes to the boards occurred for different reasons, often related to circumstances specific to an individual or what was happening with EV at the time. Some of these reasons include:

- An inability to significantly contribute to board work because of recusals on any FTX-related business.

- A mixture of burnout and wanting to reallocate their time to other high-impact activities.

- A claim of misconduct surfacing that the board subsequently investigated.

- Disagreements with the board of EV and EA leadership.

The selection and vetting process for new board members also changed over this time period. Selection criteria now place relatively more emphasis on operational experience compared to the prior focus on fields like philosophy and familiarity with EA. That said, it’s still very important for a board member to have sufficient EA context, particularly as they may need to think through trade-offs that concern the broader EA ecosystem. Integrity also became a significantly more explicit criterion in selecting board members.

Our most recent vetting process included:

- Interviews with current board members

- A conflict-of-interests declaration in which candidates are provided with a series of prompts to help identify and declare COIs

- A candidate self-reflection exercise asking them to identify potential controversies or PR issues that may arise

- Consulting CEA’s Community Health team

- An objection window for project leads (e.g. CEOs and Executive Directors) of EV projects — we let project leads know about finalists and they have the opportunity to raise concerns

- A character reference check with someone they identify they have previously collaborated with

- EV-initiated reference checks with people whom we know have worked with the candidates

- A social media review

Ongoing considerations

Having significant turnover on a board has some disadvantages. Board members with experience have been battle-hardened, so to speak, and bring experience from past situations or crises they’ve helped handle. Longer-standing board members can also bring more institutional memory and knowledge to their decision-making.

On the other hand, new board members can bring fresh eyes and perspectives that help EV notice important areas of improvement and avoid repeating past mistakes.

Another consideration when discussing board turnover is the difficulty and demands of board roles. The recent burden of responsibility for board members of EV US and UK has been much higher and more demanding than what the average board member at a nonprofit or charity takes on. As an example, even after CEOs were brought in, the boards still had hour-long meetings twice a week for many months (on top of other responsibilities that happened outside of meetings); only recently has work slowed enough that we have managed to average below one hour of meetings per week. The combination of demanding responsibilities, high levels of external scrutiny, and high stakes can make it difficult to find people who are interested in the role. I think it’s worth considering compensating trustees for their time, but it doesn’t help that in the UK, it is extremely difficult to pay charity board members for their work.

I also think the current EV US and EV UK boards (with four and three members respectively) are smaller than would be optimal if EV were going to continue operating indefinitely. While boards that are too large can make it difficult to corral all of the necessary decision-makers, small boards risk making it difficult to operate if someone has a COI, resigns, or otherwise can’t participate in a vote. My current plan is for CEA to have five board members once we spin out from EV.

Another suboptimal dynamic that the new boards are currently addressing is the supervision of CEOs and project leads. Project-level supervision has improved in some significant ways, in particular via deeper engagement with project budgeting. At the same time, board focus is still focused primarily on EV as a whole, and I think that each project would ideally have more proactive engagement and support from a board. I see this as a significant advantage of projects having their own boards. If EV were going to continue as a fiscal sponsor indefinitely, I think it would be worth experimenting with other governance structures, e.g. having advisory boards for each project.

See Julia Wise’s Advice for EA boards for more board advice tailored to an EA context. (Although advice not tailored to an EA context will be helpful for boards too!)

FTX-related investigations

Background context

EV had ties to FTX and Sam Bankman-Fried at the time of the collapse, including receiving funding from the FTX Foundation and two EV trustees also holding positions at FTX Foundation. Both EV UK and EV US agreed to settlements with the FTX bankruptcy estate. Trustees Nick Beckstead and Will MacAskill, who were respectively the CEO of and an advisor to FTX Foundation, were recused from all FTX-related discussions.

There have been calls from members of the community for further investigations into the relationship between EA and FTX. You can see variations on this proposal posted on the EA Forum linked in the Appendix.

What actions were taken and why

EV commissioned an independent investigation about the relationship between EV and FTX from the law firm Mintz, which concluded in September 2023 (and was announced by me on the Forum in December 2023 and followed by a statement from Mintz).

The investigation served multiple purposes and is an example of a project initiated by many stakeholders who put different emphases on different reasons. Much of the reasoning stemmed from a lack of knowledge on what had actually happened at FTX and who was involved. Some of the justifications included:

- Preparing for potential legal action. At the time of the collapse, EV’s leadership was unsure what legal action the FTX-estate might have pursued and also unsure of what action may have occurred at EV. Knowing the facts would better enable EV to respond to legal action.

- Demonstrating appropriate proactivity to the Charity Commission. In the UK, the Charity Commission looks significantly more favorably upon charities that are proactive in dealing with issues. EV UK wanted to live up to its responsibilities and find any issues in its own past interactions with FTX, so that it could make any necessary changes for the future.

- Identifying whether corrective action was needed. EV’s leadership wanted to know if anyone at EV had been involved in FTX-related wrongdoing or had taken other actions that should affect whether or not they should be in influential positions.

The investigation included dozens of interviews as well as reviews of tens of thousands of messages and documents. Mintz found no evidence that anyone at EV (including employees, leaders of EV-sponsored projects, and trustees) was aware of the criminal fraud of which Sam Bankman-Fried has now been convicted.

We have not and are not planning to publish any additional details regarding the investigation. Doing so could reveal information from people who have not consented to their confidences being publicized and could waive important legal privileges that we do not intend to waive.

Ongoing considerations

I’m not currently convinced that EV or CEA should invest resources into running something like a public investigation.

Different people see different reasons for conducting further investigation, which I think can roughly be sorted into two broad categories of goals:

- Help rebuild trust within the community and credibly signal to external observers that relevant misdeeds have been uncovered. This would include things like:

- Identifying potentially untrustworthy or at least blameworthy individuals and/or organizations in the EA community in order to update on their competency, limit their power, or disavow them.

- Assuaging harmful lingering doubts among the community and the general public that all important mistakes or wrongdoing by people and organizations in EA have been uncovered, which would depend on an independent and public process that would be legible and credible to external observers.

- Help improve EA culture and practices by uncovering actionable information. This would include things like:

- Knowing how the EA ecosystem might have contributed to the harms caused by FTX, which would be necessary to evaluate EA community norms or culture and understand whether and what kind of broad reforms are needed (or to understand if the EA ecosystem should be considered as net negative).

- Strengthening systems and practices in EA in order to prevent or minimize the harms that will result from the cases where, inevitably, someone (or some organization) makes mistakes in a high-stakes area. For that, we would need to diagnose the systems-level issues that have allowed mistakes to cause harm in the past, for instance by conducting something like a “blameless postmortem.” (This Asterisk piece discusses how the aviation industry came to rely on this kind of approach, and how it’s applied.)

Optimizing for different goals would mean running different versions of an investigation. For instance, investigations aimed at the first set of goals might focus on individuals, trying to find out who knew what and when. An investigation aimed at the second set of goals might take a more structural approach, trying to better understand what happened at FTX and what processes in EA might have mitigated the resulting issues.

I don’t think an investigation is likely to be successful in achieving either of these sets of goals. To uncover novel actionable information about what happened at FTX would depend on an investigator having access to substantive information not found or made public by the extensive legal proceedings or the many authors and journalists who have reported on this story. One barrier to finding novel information is that so much has already been reported, both inside and outside of the EA community. In some conversations I’ve had with people who were interested in further investigation, I realized that they weren’t aware of all of the information that was already public (which I think is very reasonable given how confusing the situation is and how the information isn’t centralized), which is one of the reasons we’ve gathered links to various information in the Appendix. I don’t think that information paints a definitive account of what happened or why. But I also think that’s an unrealistic standard for such a complex story. We have only partial accounts from different actors, many of whom we have reason to be skeptical of.

Any novel and action-oriented reporting would likely require an investigator to get access to sensitive and privately held information from individuals. However, rebuilding community trust would depend on that investigator being able to publicly share the information they learned, and much of the theoretically relevant information would be held by individuals who are not incentivized to cooperate, whether because of legal or reputational risks, or the threat of public criticism. I expect that in exchange for receiving information an investigator would need to commit to communicating their findings in a non-detailed and anonymized fashion, which would undermine the attempt to make legible and credible claims to have been rigorous, comprehensive, and impartial.

I don’t think an investigator from within EV, CEA, or other established EA organizations would be considered a credible enough investigator of those organizations or their staff to satisfy some skeptical audiences. At the same time, I’m skeptical a non-EA investigator would produce nuanced findings or conclusions compelling to the community. Our distinctive community dynamics are hard for external observers to navigate and our standards for evidence and reasoning are unusually high.[4]

If individuals do have information related to FTX they want to share, they can do so regardless of whether an investigation has taken place. Many individuals already have (Appendix). In addition, EV has updated its communication policy so it is no longer blocking anyone from sharing relevant information.

It’s possible that the probability of success is higher than I think, and I can imagine some arguing that it’s worth pursuing even with a very low probability of success. With that being said, trying to run an investigation like this would be costly in terms of time and money (for context, the legal fees for the Mintz investigation and related work were over $750,000, which does not also count the extensive additional costs associated with time spent by EV staff), and in my assessment there are better ways for us to use those resources.

I am excited about efforts to strengthen EA culture and practices (which is part of the motivation for sharing actions taken by EV in this post and will continue to be part of the motivation for CEA’s stewardship of EA), but I don’t think an investigation is necessary for or likely to help with these endeavors. I think posts like this one and ones others have written (Appendix) can help identify updates the community should consider to reduce the risks from FTX-like incidents.

Instituting financial reforms

Background context

I think that pre-FTX EV was not living up to the standard of financial rigor we should hold ourselves to as a collection of projects that operate globally with a cumulative budget over $100 million.

One embarrassing example worth sharing as a lesson learned: in 2022, some EV projects spent money that had only been promised from the FTX Foundation, although they hadn’t actually received that funding yet. That effectively meant that these projects were spending unrestricted funding that had not yet been committed to any of the projects. EV also didn’t have a clear process in place for what would happen if a project ran out of funding allocated to it. This was a clear mistake, and we have created policies to prevent similar incidents.[5]

As EV untangled itself from the FTX crisis, it was clear that it needed strict financial reforms and oversight. EV was in a financial crisis; it had banked on receiving millions from FTX over the coming years and faced the prospect of claims from the FTX estate over the funding it had already received (see resulting settlement).

What actions were taken and why

In response to our scrutiny of EV’s financial systems following the FTX collapse, in the midst of EV's financial crisis, we instituted better financial controls and put in place more experienced finance leaders.

Some examples of the financial controls implemented include:

- Guardrails to prevent projects from running out of funding in a disorderly way and runway requirements to maintain resilience to possible future crises.

- Improved budgeting practices, better policies and processes for expenses and donations, and clarified conditions under which projects can and cannot spend money.

EV US also changed its financial auditing service to Moss Adams, resulting in better advice compared to previous years.

Ongoing considerations

- Housing multiple projects under one roof creates complicated financial challenges. If one project accepts money from a source that later turns out to be suspicious and faces legal action, EV as a whole becomes entangled in the legal action, impacting all projects.

- There are still improvements to our financial controls identified by EV's auditors that are currently being implemented, such as more and better reconciliations.

- Projects would ideally have more access to expert financial advice that is timely and tailored to their particular needs, but EV’s bandwidth constraints currently make that impractical.

Improving donor due diligence

Background context

EV accepted money from FTX-related sources, which later turned out to be money from a company that has been found to have engaged in large-scale fraud. Based on an independent investigation, I’m confident nobody at EV knew about this fraud. Both EV UK and EV US agreed to settlements with the FTX bankruptcy estate.

EV had a donor due diligence policy prior to November 2022, but it is unclear to me how much effort was put into proactively researching and addressing potential donor issues.

What actions were taken and why

After learning about FTX’s fraud, EV instituted a better donor due diligence process that requires checking the background of all people who donate or seem likely to donate more than $50K to EV or its individual projects (for context, a donation of $50k would represent less than 0.1% of the total funding the EV entities received in 2023).

EV also now has a lower bar for what warrants caution about whether to accept a donor's money. (This caution could also imply returning a donor's money if it has already been donated, although EV has yet to return a donation because of due diligence concerns.) Some decisions to not accept funds from someone are based on clear facts (e.g., public reporting on past misconduct), while others are based on broader judgments of a person's character that may not involve evidence of criminal activity. Compared to the pre-FTX era, we’re more likely to take character judgments into account when assessing donors.

EV also maintains an internal list of people from whom we will not accept money, which influences where our constituent projects go to fundraise. In at least one case, an EV project chose not to fundraise from someone because of our updated processes.

The heightened focus on donor due diligence is a direct result of EV being hurt by accepting money from Sam Bankman-Fried and FTX, and I think this change is good. However, I still think it’s unlikely that our current level of donor due diligence would have discovered that FTX was committing large-scale fraud. I think you would have needed (at least) financial audits from experts for that.

Ongoing considerations

- While donor due diligence is helpful, it isn’t a magic bullet. Charities have limited visibility into the people and organizations that they accept donations from, and it is hard to be 100% confident we are getting it right. However, we are currently erring somewhat (but not totally) on the side of being conservative when it comes to potential major donors.

- The external donor due diligence tool we use (LSEG World Check One) primarily relies on existing legal investigations and reports of misbehavior. If a fraudulent or otherwise problematic individual hasn't been caught by the legal system, EV's donor due diligence tools may not catch them either.

- While EV sometimes can receive non-public information about potential donors, we may not receive all relevant information, and we may also receive information of low or unclear quality.

- A threshold lower than $50k could be better, although I currently don’t think so. This could be operationally challenging given EV’s current size and operational resources, but may be more plausible for our projects when they are operating independently. I wouldn’t encourage other organizations to copy our threshold without thinking through their particular organizational needs.

- EV’s list of donors it would not accept money from is centralized, and not everyone working on fundraising at all projects at EV are aware of everyone on the list. While such a donation would eventually be caught by someone at EV, it’s possible that someone at a project could have already invested significant amounts of time and relationship capital into raising funds. To the best of my knowledge, this is a theoretical issue that has not yet occurred. I expect this to be much easier for projects to manage once they are independent and can make their own determinations of whom they should accept money from.

Adopting a restrictive communications policy

Background context

I was not the primary person who designed the communications policies, so this section in particular involves me piecing together different components from different people. Some of the decisions discussed here were made before I joined EV in January 2023, and because others had more context we settled on a division of labor in which I mostly deferred on communications policies (which might have been a mistake in itself, though when I did spend some time trying to get up to speed on the reasoning behind the decisions, my views moved closer to those who had made policy decisions).

What actions were taken and why

In the months after FTX, EV adopted a communications policy that placed restrictions on staff and board members' external communication (EA Forum posts, podcast appearances, etc.). In November and December 2022, this new communications policy meant that all public communications related to FTX needed to go through a central approval process. Shakeel Hashim, then CEA’s Head of Communications, posted about this on the EA Forum in November. The policy was updated and loosened a bit in late December. In February 2023, the restrictions were reduced more significantly: staff only needed approval if commenting on EV’s relationship with FTX or EV’s legal structure (there was also some pre-approved language).

The current EV communications policy only requires approval for comments on the details of the FTX settlement and legal implications for either EV or other EV grantees, or EV’s legal structure (and there is still some pre-approved language). Its intent is to make sure staff are only saying accurate things about complex and sensitive legal issues.

There isn’t a singular “why” to any of these decisions, as there wasn’t a singular decision-maker. EV US and EV UK collaborated to make them, which originally involved two sets of boards and would later also involve two CEOs. Different individuals put different weights on different reasons.

The original communications policy was a direct response to the FTX collapse. Our lawyers repeatedly and strongly advised us that issuing public statements carried significant legal risk, which matched our sense of general legal best practice. EA norms are significantly different than legal norms, and adversarial lawyers are generally significantly more interested in money and a favorable outcome for their clients than truth-seeking. The bankruptcy lawyers you are up against follow no principle of charity — they are paid to get as much money from you as possible. From a legal perspective, it’s often best to be quiet if you’re in a crisis that carries the risks of lawsuits from actors who may be incentivized to portray you negatively.

Our approach to risk mitigation overall (including but not limited to the communications policy) intentionally erred toward conservatism. This was largely due to the correlated nature of risks at EV, where speaking about FTX might be a priority for a subset of EV projects, but the legal risks incurred would accrue to all of the projects, including ones that don’t place much value on speaking about FTX. For example, while CEA or an individual affiliated with EV (like Will MacAskill) may have wanted to say more about FTX, from the perspective of some other projects, EV staff members talking publicly and freely about FTX wouldn’t help advance their mission while incurring costs and risks. The decoupling of risk is one of many reasons I am glad that EV is shutting down and projects will become independent.

We also didn’t want staff to accidentally say something inaccurate or confusing that could be used by adversarial parties. Until our independent investigation was complete (described here), we didn’t know what we didn’t know. Even seemingly simple questions like “how much of FTX’s money do you have” took time to figure out, as it involved complicated financial questions around which money was in which EV entity, which entities related to FTX counted in that equation (e.g. Alameda), how much money attributable to FTX had already been spent, and the status of money that the FTX Future Fund had promised to transfer but had not yet reached EV’s bank accounts.

There were also difficulties in communicating internally to staff about the nature of FTX-related risks. We didn’t want to violate privilege in a way that could later be exploited by an adversarial party. These difficulties were further exacerbated by the complicated legal structure of EV US and EV UK, where each organization not only had to understand (A) how legal privilege worked within their own organization, but also (B) how legal privilege worked when sharing information with another collaborative organization, and (C) how that privilege might be affected by the fact that EV US and EV UK operated in two different legal jurisdictions with two different sets of laws governing privilege. The US and UK’s legal systems are also set up differently, such that less information is privileged in the UK than in the US, but the UK is also generally a less litigious society. Waiving privilege risked being a lowest-common-denominator situation where the more limited privilege rules may apply from the UK but the stronger legal risks could apply from the US. This intersection of multiple jurisdictions was particularly difficult to navigate.

Understanding how legal privilege worked took a significant amount of time and money. Moreover, I’ve been told that some people at EV believe the legal advice they originally received about privilege was inaccurate, further slowing down the process of loosening the communications policy. These challenges also made it more difficult to disseminate information within the organization, including correcting potential misconceptions.

With that being said, we were fairly confident along the way that the communications policy was too conservative — and we knew it was costly. This was in part because when we did take time to press our external counsel for greater clarity on their reasoning, we frequently found that their advice was overly broad. Moreover, we were repeatedly able to find additional areas to carve out where communication risks were not as high. We felt this was partly because external counsel wasn’t always trying to give us nuanced advice, and partly because we felt that our lawyers likely weren’t accounting for all of the non-legal benefits that could come from a less restrictive communications policy. However, it was hard for us to understand the specific ways in which the policy might be too conservative, and we didn’t want to toss it all out as some communications restrictions seemed warranted. Because the group of people who could actually invest in changing the communications policy had very little spare capacity, we had to make difficult trade-offs on what to prioritize. Given the immense time it took for us to understand the relevant legal nuances, we often prioritized other important and urgent tasks.

Ongoing considerations

This was the policy that was at least partly responsible for prominent figures in EA, especially those affiliated with EV, not making many public statements on the EA Forum. Will MacAskill, then a board member of EV UK, is an example. As Will writes, he tried numerous times to post something, and our legal counsel strongly advised us not to permit this (though the reasons why were complicated and partially related to the investigation that was occurring). It seems likely to me that if individuals had also sought their own independent personal legal counsel they would have received the same advice (i.e. not to talk publicly), though those individuals may have weighed their own personal trade-offs differently.

In hindsight, I think we made some wrong judgment calls about this policy. Here are some ways in which I think we might have made mistakes:

- One person involved with crafting and interpreting the policy told me that they feel that they mistakenly spent too much time trying to unblock projects on specific communications or actions they wanted to take. They said that they should have deprioritized that in favor of developing a deep understanding of the legal issues involved in order to update the policy as a whole. In general, I think EV made a mistake by not prioritizing understanding privilege sooner (though that was not the only legal reason why communications were restricted). I’d recommend that as part of good crisis prep, other organizations get simple legal guidance to help them understand privilege in the jurisdictions that are relevant to them before any crises occur so they don’t need to scramble when crises happen.

- We repeatedly underestimated how long the relevant legal proceedings would take, and therefore how long EV staff and board members would be unable to openly talk about FTX. This means we underestimated the costs of this comms policy.

- We also could have done a better job at internally communicating changes to the policy. When we later loosened the policy, we received feedback that some staff were scared or confused and thus continued to err on the side of conservatism. Even in the process of writing this report, we realized there were still some aspects of the updated policy we needed to revise and clarify (which we have since done).

- I think we should have communicated more clearly about the policy in public. Becca Kagan and Owen Cotton-Barratt had previously discussed their intent to say more about the communications policy, but both of them ended up resigning from their respective boards shortly thereafter and were no longer in a good position to share this information. I later intended to finish drafts that they had started, but ended up deprioritizing it as I realized it was more complicated than I had originally understood and different crisis response priorities competed for my time. This is one reason among others why I wish we had invested more in bringing on additional capacity.

This policy had unavoidable tradeoffs between reducing legal and financial risk and sharing information openly. It is true that we both frequently followed legal advice and that we said more than our lawyers sometimes wanted us to. Nonetheless, I think the policy seriously worsened community sense-making post-FTX, negatively affected many individuals affiliated with EV, and contributed to a loss of trust in prominent EA figures and institutions — and this is true whether or not we generally made the right calls overall. People were understandably confused as to why they weren’t hearing more from the people who knew the most about the situation. This restrictive comms policy also stood in contrast to the EA community’s culture of transparent reasoning and public debate. While I think the EA community sometimes errs too far on the side of public disclosure, I think the overall desire for truth-seeking is an unusual and valuable strength of the EA community that I value, and I’m saddened when decisions trade off against it.

But overall, I feel very unsure if adopting a strict comms policy was a mistake. It seems plausible to me that it protected individuals and institutions from undeserved lawsuits and settlements, and we had to make these decisions under challenging circumstances of uncertainty and extreme urgency. Board members and EV executive staff didn’t have much legal experience ourselves, and we didn’t have time to form our own views about the legal arguments against communicating publicly. So in practice, we were making a decision between following legal advice or overruling it without a strong inside view, and erring on the side of deferring to the experts in an area where the more EA-aligned decision-makers don’t have relevant background generally seems like a good heuristic to me. Nevertheless, this policy had significant costs, and I think it’s reasonable to critique it for its stifling effect on the community. I hope we never have to institute a policy like this again.

Streamlining whistleblowing policies

Background context

Effective Ventures (EV) has long had a whistleblowing policy in place, but it lacked clear procedures. Some employees may not have been aware of its existence. EV’s policies and processes were probably about as good as is normal for most organizations, but I think streamlining the whistleblowing process was important so that employees feel capable and protected when raising legitimate and important concerns.

What actions were taken and why

EV updated its whistleblowing policies to better protect whistleblowers and reduce the fear or friction that could prevent people from speaking up about potentially important issues. This was done through a series of small design improvements, such as ensuring that the whistleblowing policy is easily findable, that employees are aware of it, and that there are multiple points of contact to raise concerns to. The points of contact purposefully include one male-identifying and one female-identifying contact, as well as people with varying degrees of involvement with the EA community.

Additionally, EV set up emails and forms for staff to directly and anonymously reach out to the EV US and UK boards and shared an independent avenue to get whistleblowing advice with EV UK staff.

EV also clarified what isn’t part of the whistleblowing policy. For example, while we care about confidentiality and will work to maintain it when desired, we want to be explicit that we aren't promising absolute confidentiality. Whistleblowers’ identities may become known if that information is essential to the investigation progressing, particularly if required by law.

Ongoing considerations

- EV has deprioritized regular reminders about this and other policies while we’re offboarding projects. I expect CEA to facilitate better ongoing reminders of key policies with staff once CEA has spun out, and I hope other projects do so as well.

- Making whistleblowing easier to do could lead to abuse of the system. I haven’t seen any evidence of abuse of EV’s policies, though I have seen messages from people external to EV that raise complaints of questionable quality and that are potentially bad faith.

- As part of a project on institutional reforms in EA, Julia Wise researched resources on whistleblowing.

Updating anti-harassment and misconduct policies

Background context

The revision of EV's anti-harassment and misconduct policies was prompted by allegations of sexual misconduct against Owen Cotton-Barratt, an EV UK board member. An independent investigation solicited by the UK and US boards and conducted by a law firm additionally provided evidence of misconduct.

When the allegations against Owen publicly surfaced in early 2022, a “review and revise” workflow was already underway for the misconduct and anti-harassment policies, and these allegations made editing the anti-harassment policies one of the highest priorities for the EV executive team.

What actions were taken and why

EV US and UK updated their misconduct policies, keeping in mind the following priorities:

- Reducing risks of misconduct. We want to protect our staff, contractors, and community.

- Creating fair processes. We want to be able to act quickly on cases where the facts and judgments are clear, but it’s also important to ensure fair processes, particularly as facts can oftentimes be messy.

- Clarity. People should be able to easily understand how to comply with the policies and what their options are if they experience or learn of misconduct; the policies should not read as incomprehensible legalese.

- Implementation. Not only should policies exist, but there should be a clear and practical process to implement them. For example, if you approach a designated contact person, that person should know how to respond.

- Comfort. These topics can feel scary, and we want people to feel comfortable coming forward with relevant information.

- Legal compliance. In addition to protecting the legal status of our two entities, it can also help build trust in our institutional processes.

- Speed. We don’t want to make the perfect the enemy of the good, and it was probably worth getting out incremental improvements, even if we might need to update them later.

Some specific changes we made to the anti-harassment and misconduct policies include:

- Adding more points of contact to report harassment or misconduct to

- Clarifying situations that would and wouldn't be escalated

- Creating a feedback email and an anonymous form to send information directly to the EV executive team

These changes were developed based on advice from external legal counsel and feedback from each of EV’s fiscally sponsored projects. The EV executive team also solicited best practices from other organizations that have experience with preventing and responding to misconduct, but I don’t remember how much these best practices ultimately influenced EV’s policies.

Ongoing considerations

The misconduct policy could still be more clear and accessible. EV has a misconduct policy, grievance policy, and an anti-harassment policy, and the process of identifying which exact policy and escalation process is most relevant to a given situation might be confusing for a staff member on the fence of reporting something.

Improving the COI policy

Background context

EV had suboptimal conflict-of-interest (COI) policies and processes in the past. For instance, some board members had relationships with the FTX Foundation, which could potentially bias them. (Nick Beckstead was the CEO of the FTX Foundation, and Will MacAskill was an advisor.) Although a COI policy existed, it wasn't regularly discussed, and there were no robust mechanisms to ensure that COIs were regularly reported. Additionally, the board culture didn't incentivize other board members to encourage each other to recuse themselves from decisions that might involve COIs. That said, the Charity Commission inquiry found no evidence to suggest that there were any unmanaged conflicts of interest regarding funds the charity received from the FTX Foundation or that any trustee had acted in a way contrary to the interests of the charity.

What actions were taken and why

EV formalized conflict-of-interest reporting for board members and CEOs of EV US and EV UK and implemented processes to make it more likely that these COIs are kept up to date. New board members now have to complete forms detailing possible sources of COIs, such as investments, gifts, or hospitality received from third parties, and close relationships with anyone at EV or a closely related entity.

Mechanisms have been put in place to ensure that board members continue to report their conflicts of interest. For example, whenever the boards vote on something, they are asked to disclose any relevant COIs. There are also annual reminders to report new COIs. We have successfully changed the culture around COIs, with board members frequently recusing themselves even when our new stricter policies don't say that they have to, and according to a board member who was present before November 2022, board members feel more comfortable nudging one another to consider recusing themselves from board decisions if COIs may be involved.

Furthermore, EV mandated the reporting of all staff's personal relationships within a project and between projects if it affects hiring, grantmaking, or management.

Ongoing considerations

- There is a trade-off between recruiting board members with EA context and minimizing COIs. Context on the EA ecosystem is valuable for some board decisions, but this context correlates with the risk of COIs, especially given the potential overlap between social and professional relationships in EA. Minimizing CEOs’ and board members’ COIs is also made harder because hiring people for these roles is difficult, with a small pool of eligible and willing candidates.

- While I have seen multiple instances of COIs being proactively addressed by staff within projects, I think it will require active effort to ensure that addressing COIs stays an ongoing cultural concern as we move further away in time from FTX’s collapse.

- I am slightly worried that there has been an overcorrection from the board on recusals and declaring COIs. I think board members are attempting to hold themselves to strict standards of integrity, which I deeply appreciate, but I also worry that at times there may be more recusals than needed which could deprive us of valuable input and votes.

Clarifying the level of separation between the EV US and EV UK entities

Background context

Charity law works differently in different countries. Typically, charities need to fulfill specific legal requirements in order to get official status as a charity in a given jurisdiction. To give you a sense of how this works: what people often refer to as “the charity Oxfam” is actually a “confederation” of 21 affiliates — independent member organizations. They apparently have 22 CEOs — one CEO (and one board) for each affiliate, plus an additional international Executive Director and international board.

EV UK and EV US are separate legal entities, which collaborate together to support our projects. Among other things, this structure enables projects to hire staff and accept tax-deductible donations in both the UK and the US. (See Background on EV for more detail.)

What actions were taken and why

In December 2022, Effective Ventures improved and clarified the level of independence between EV US and EV UK. The two charities kept working closely together, but the boards of both entities appointed their own CEOs and made many operational improvements.

We also changed our internal and external communication to make it clearer that EV US and EV UK were affiliated yet independent entities. As an example of one of the reforms taken, we created a formal written document called an “affiliation agreement” that detailed governance norms such as board independence, resource sharing, and inter-institutional communication norms.

This reform wasn’t directly caused by the collapse of FTX, but was triggered by EV’s increased focus on governance and careful legal compliance in the aftermath. In particular, unclear governance structures increased the chance of regulatory confusion (which could in turn result in significant time and legal fees being spent addressing regulatory concerns). This is important as regulators understandably want to know that institutions under their jurisdiction are following their regulations, which are not necessarily the same as those in other jurisdictions.

This was an extremely large undertaking with significant time, monetary, and coordination costs. It also serves as an important example of a reform that could and should have been taken long before FTX collapsed. Undergoing these reforms would have been significantly easier and less stressful to do without other reforms to implement simultaneously or EV UK being under investigation from the Charity Commission. Moreover, it costs more in legal fees to have lawyers move more quickly, and it would have been easier and less costly to solicit legal advice had it been done earlier. It was also difficult to find staff who were willing to work on this and other related projects, as the degree of stress involved was high. I had one person I spoke with tell me they were excited about a career that focused more on writing policies like the type EV needed, but they were understandably reluctant to work on such policies in an environment with intense regulatory scrutiny.

Ongoing considerations

- Having two boards and two CEOs increases the chance of significant friction, particularly during times of crisis when decisive action is required. I think hiring CEOs was a meaningful improvement over having the boards be the primary decision makers, as it reduced the number of decision makers from seven to two. Hiring CEOs who communicate well with each other and building capable teams that will help the boards and CEOs move forward in areas where collaboration is required is very important. In practice, I think Howie and I disagreed remarkably little, and I think Rob and I have a similarly collaborative relationship, in part because Rob and I were selected for our ability to collaborate with the existing CEO. Nevertheless, I think the coordination costs of a multi-entity organizational structure are worth weighing seriously against their benefits.

- The operational intricacies of figuring out the best procedures and relationships between two entities and the many internationally operating projects played a role in deciding to shut down EV. As projects set up their new entities in preparation to spin out, they’re thinking through what structures make sense for them.

Initiating EV shut down

Background context

See Background on EV (and the rest of this post!) for more historical info.

What actions were taken and why

The EV US and EV UK boards have decided to spin out all of EV's projects and EV will not start sponsoring new ones. This process began towards the end of 2023 and is expected to take up to 2 years to complete in full. It's unclear exactly what will happen to the EV US and EV UK legal entities, although it's likely that they will gradually wind down and dissolve.

Several factors contributed to the decision to wind down EV, such as:

- The majority of the projects expressed a desire to spin out.

Allowing projects to set up independent entities will decorrelate any legal, reputational, or financial risks between projects, and I think it will help to build a more robust and resilient EA ecosystem.[6]

- Large differences in operational needs and risk appetites across organizations made it challenging to make EV-wide policy decisions, as projects often experience very different costs and benefits. For example, some projects would prefer a comms-forward, EA-coded strategy, while others depend less on public outreach and have no explicit EA branding. This was exacerbated by not having or communicating a clear point of view on EV’s overall risk profile.

- Separating into smaller, more cohesive organizations reduces overall legal risks and attention. The more money you hold, the more of a lawsuit target you become, and EV has historically held a lot of money. This risk is exacerbated if you have more people doing different things, which increases your attack surface and the number of actors who could plausibly have an incentive to sue you. And if someone sues your organization because of an action taken by one of the projects, all the other projects also bear the costs.

- Individual projects could benefit from more board supervision than what naturally happened with EV’s legal structure. EV board members have often spent significantly more time on their board responsibilities than typical non-profit board members do, while simultaneously spending less time per EV project than typical non-profit board members spend on their non-profit.

- Board members and EV executives, myself included, think that spinning out projects will not significantly diminish their impact on the world. Still, I do think it creates an additional burden on some projects to run their own operations, which can be particularly challenging for smaller organizations.

- I still think there is a role in the world for fiscal sponsors that can host EA-aligned projects. But given the overall baggage of EV and its structural flaws — e.g. I think it may be possible to create a different entity structure that doesn’t necessitate two parallel sets of boards and CEOs — I think it would be better to start anew than to reform EV.

When organizations spin out, they will be able to use EV policies and best practices as the basis for their own policies and institutional norms. Some organizations may significantly revise their policies to meet their own needs, while I expect some will adopt something very similar to EV's policies.

Ongoing considerations

This process will take significant amounts of time to complete. Spinning out all projects is expected to take up to 2 years because the EV team and the project leads want to ensure that the new entities are set up well. Decisions about legal structures and organizational configurations are important to get right the first time, as they can be difficult to change later. Plus, setting up a charitable entity typically takes longer than setting up a corporation.

I also think there is real demand for alternative options for fiscal sponsorship, and sometimes organizations may insufficiently explore sponsorship options that are not part of the EA ecosystem. I think it would probably be good if someone were to responsibly set up and run a fiscal sponsorship organization, though I think it is difficult to do so well. I hope that some of the information in this post can help someone if they do choose to pursue such a project. If someone wants further advice, they can feel free to reach out to me, though I may have limited bandwidth to engage.

Some of the lessons EA can learn from the EV experience

Some of the challenges faced and actions taken by EV were specific to our particular context, but many were not. There’s an opportunity to learn from our experience. The list below probably isn't exhaustive, but it’s a good place to start.

Brief summary of these lessons

- Organizational governance and compliance can have serious implications

- It’s important to carefully think through and explicitly communicate your organizational risk strategy, and pay attention to it as your organization develops. This is particularly true for a fiscal sponsor

- EA organizations often underrate experience relative to “intelligence” and “value alignment”

- Vetting external counsel is important

- Crisis prep is underrated relative to crisis response

- Communicate early (and have the resources to do so)

- Invest in capacity building early

The lessons

Organizational governance and compliance can have serious implications

As a baseline, it’s important to recognize the implications of organizational governance aspects like how you set up your organization, how your organization interacts with its board, when to seek legal advice, and how your policies relate to local regulations. Organizational governance isn’t always sexy, but the boring details matter, both internally (e.g. establishing structures that can scale effectively) and externally (e.g. implementing policies that are compliant with local regulations in multiple jurisdictions). Not thinking carefully about governance can come back and bite you (whether through reputational damage, regulatory scrutiny, or requiring more effort to overhaul than to establish at the outset), particularly during periods of heightened scrutiny when you may already be strapped for organizational resources.

It’s important to carefully think through and explicitly communicate your organizational risk strategy, and pay attention to it as your organization develops. This is particularly true for a fiscal sponsor

Some people will look at the list of reforms described in this document and think that it goes overboard. For some organizations, they may be right. It’s common advice for startups not to be overly focused on compliance as they’re getting their organization up and running. However, if you are running an organization of a large enough scale or with enough of a public footprint (e.g. because you are trying to or liable to attract media attention), then it is worth investing more in ensuring your legal and operational practices are sound.

Some activities (like communicating a lot or very transparently) and operational decisions (like setting up a complex legal entity in order to facilitate hiring or grantmaking) are also inherently harder to navigate without incurring some level of risk. Many organizations or projects knowingly take on those risks because the benefits are sufficiently valuable to them, but other organizations might value those benefits less or generally be less risk-tolerant. An organization’s risk profile — the risks it takes on and how conservative it is when engaging in potentially risky areas — should match its needs and theory of change.

EV historically didn't have a particular philosophy to approaching risk in mind and didn’t communicate a risk strategy to projects when they joined. As a result, there were many different risk profiles that collectively made the risk profile of EV more difficult to navigate than it needed to be (e.g. some orgs were grantmaking orgs while most weren't; some orgs had a very comms-forward strategy while others didn't). This meant that the reforms taken in the aftermath of FTX were oftentimes a compromise that made different projects unhappy in different ways. It also meant that these reforms felt unpredictable to the projects, because they hadn’t realized what overall risk profile EV had when they joined.

EA organizations often underrate experience relative to “intelligence” and “value alignment”

Prior to joining EV, I felt that I valued formal training and professional experience more than many others in EA, and I now believe even more strongly that this is under-valued by many organizations and decision-makers in the EA ecosystem. I think this is particularly true for areas that require significant specialized knowledge (e.g. law, finance).

I don’t think a universal approach is appropriate for all roles. It’s worth asking both how much you believe your organization’s approach should differ from an average (non-EA) organization, and how much EA context an individual will need to make tradeoffs that benefit the organization. For example:

- When I worked at Open Philanthropy, it was extremely important for cause prioritization researchers to share organizational values like scope-sensitive altruism and impartiality, as they were asked to prioritize between different potential giving opportunities, and that values used to make those decisions were oftentimes different than those that would be used by your average researcher or foundation.

- In accounting, there are processes and best practices that many people in the world have deep expertise in, as a product of years of formal training and professional experience. By contrast, even highly intelligent and EA-aligned generalists will be unable to provide the same level of expertise. It’s likely that these established approaches are suitable for most EA organizations, so it’s unlikely that you should put significant effort into creating novel finance practices or attempting to figure them out from first principles. If you want your accounting to be correct and make sure that it’s compliant, it’s likely worth hiring an expert.